What Happens When The Bet Against America Fails?

There’s a narrative sweeping through markets right now that feels almost irresistible. The dollar is debasing. Emerging markets are finally having their moment. Central banks are selling Treasuries and buying gold. Capital is rotating out of American assets and into “the rest of the world.” Call it de-Americanization, de-dollarization, or the death of American exceptionalism. Whatever label you prefer, the thesis has achieved consensus status.

And that’s precisely why it’s dangerous.

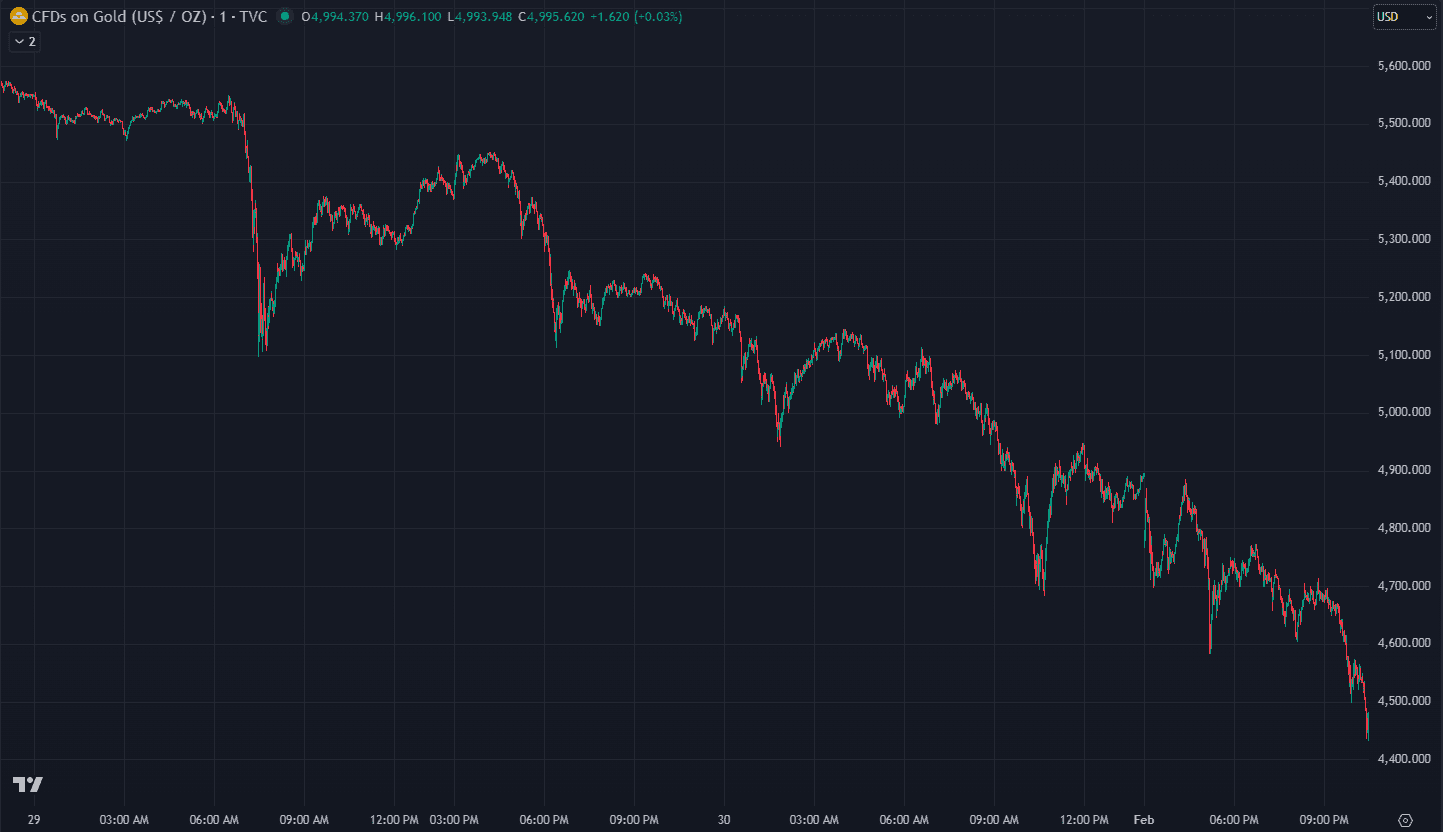

Friday’s market action offered a glimpse of what happens when crowded trades meet unexpected catalysts. Gold crashed over 12%. Silver suffered its worst single-day loss since 1980, plunging more than 30%. The precious metals complex experienced a $10 trillion swing in market cap in a single session. The dollar spiked. Emerging markets stumbled. Kevin Warsh’s nomination as Fed chair triggered the move, but the real story isn’t about one personnel decision. It’s about a positioning extreme that got toppy and was waiting for any excuse to unwind.

We don’t think the world is abandoning America. We think the de-Americanization trade has become the most crowded macro bet of 2026, and we think it’s going to reverse. In this ledger, we’ll walk through the deeper macro mechanics behind that view. Not just what we expect, but why.

The Consensus Position

Let’s start by going through just how one-sided this trade has become.

Emerging markets returned 34% in 2025, their best year since 2017. More striking still, EEM outperformed the S&P 500 by over 20% in the first sustained period of EM leadership in over a decade. Fund managers and strategists are nearly unanimous. JPMorgan says EM “hasn’t looked this compelling in 15 years.” Goldman projects another 16% return in 2026. Bank of America declared that “EM bears have gone extinct.” The greatest capital rush into emerging market securities since 2009 occurred in 2025.

Meanwhile, the dollar posted its sharpest annual decline in eight years. Gold doubled over a 12-month span. Silver nearly quadrupled. The debasement trade, a bet that the U.S. is printing itself into irrelevance, became the dominant theme across hedge funds, family offices, and retail alike.

Treasuries have also felt the pain. China’s holdings dropped to $689 billion in October, the lowest since 2008, down 47% from the 2013 peak of $1.32 trillion. Central banks globally have been accumulating gold at a pace of over 1,000 tonnes annually for three consecutive years, explicitly diversifying away from dollar reserves. The “sell America” narrative took hold.

But that’s all about to change. The only question is what triggers the reversal.

WHY THE DOLLAR STABILIZES

The de-Americanization thesis requires continued dollar weakness. But the dollar’s decline in 2025 wasn’t driven by structural collapse. It was driven by specific policy shocks whose effects have largely run their course.

The primary catalyst was Liberation Day. When the Trump administration announced sweeping reciprocal tariffs in April, markets panicked, and the sell America trade took hold for good reason. If the world can’t trade with America, why would they need as many American dollars or Treasuries? But the tariff shock has since been absorbed. Trade deals have provided a stabilizing anchor. The Xi-Trump meeting in October delivered de-escalation. A deal with India lowered Trump’s tariffs from 25% to 18%. The lower tariffs go, the more strength returns to the dollar. Markets are recalibrating, and the focus is shifting back to fundamentals, where the dollar still holds key advantages.

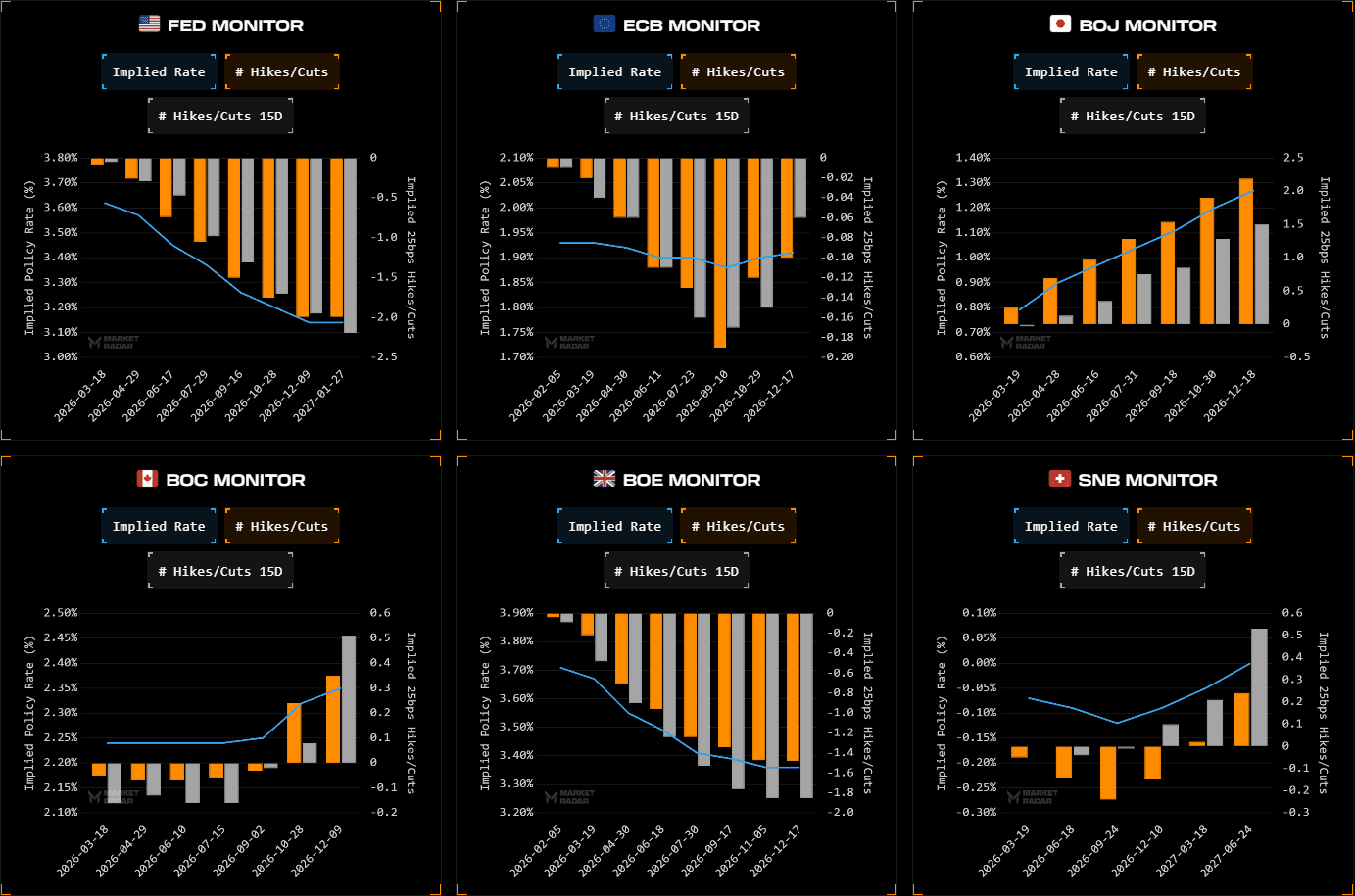

Rate differentials continue to favor the dollar. Despite 175 basis points of Fed cuts since September 2024, U.S. rates remain structurally higher than every other developed market. The Fed funds rate sits at 3.50-3.75%. The ECB is at 2% and has signaled it’s done cutting. The Bank of Japan just raised to 0.75% and might reach 1.25% by late 2026. The Swiss National Bank sits at 0%. This means U.S. Treasuries still offer a yield premium over German bunds, JGBs, gilts, and virtually every other sovereign bond market. That differential creates persistent demand for dollars through carry trades and international portfolio allocation. By March 2026, the Fed is expected to have delivered all its cuts for this easing cycle. Most other G10 central banks will be close to finishing their own cutting cycles. When rate differentials stop compressing, the primary driver of dollar weakness disappears.

For the dollar to decline, capital has to flow somewhere else. The problem is that every alternative has its own issues. Europe faces deep structural issues, with Germany attempting fiscal stimulus while France runs unsustainable deficits. The ECB has limited room to support growth if conditions deteriorate. Japan’s policy mix remains incompatible with a yen rebound. The BoJ is normalizing at a glacial pace while the government pursues reflationist policies. The 10-year JGB yield just hit 2.27%, its highest level since 1999, and according to Capital Economics, roughly 2.0 percentage points of that yield reflects inflation compensation as Japan’s economy reflates. Japanese inflation has run above the BOJ’s 2% target for 44 consecutive months. This is not yen strength, rather it’s the market demanding higher yields to compensate for persistent inflation.

And then there’s gold. This has been the best asset to own throughout this environment. But Friday exposed its vulnerability. When gold crashes over 15% and silver plunges 30% on a single nomination announcement, that’s no longer safe-haven behavior. That’s a crowded trade masquerading as one.

The dollar may not be perfect. But in the land of the blind, the one-eyed man is king. Investors fleeing the dollar have nowhere compelling to go at scale. Gold and other metals served as that release valve. We believe that’s coming to an end.

Warsh’s nomination as Fed chair signals a potential shift in monetary policy stance. He’s widely viewed as the most hawkish candidate among the finalists, someone who has criticized quantitative easing, advocated for balance sheet discipline, and prioritizes inflation control. Whether Warsh actually delivers hawkish policy is almost beside the point. What matters is that the market’s asymmetric bet on extended dollar weakness just got challenged. Warsh reintroduces the threat of monetary discipline to a market that had priced in permanent accommodation. That’s exactly what the crowded debasement trade didn’t want to see.

But here’s the nuance that matters. No Fed chair, not even Warsh, is going to sacrifice tens of trillions of dollars of stock market cap to correct inflation by 50 basis points. If inflation sits at 2.3 or 2.5%, no policymaker wants to be the one who crashes the S&P 30% to get it to 1.8%. They’ll wait for inflation to trickle back down to target rather than force the issue. The threat of hawkishness is enough to unsettle the debasement trade. The actual policy doesn’t need to be draconian.

The dollar doesn’t need to surge. It just needs to stop falling. And when the primary tailwind behind EM outperformance and metals rallies disappears, those trades reverse.

Why U.S. Growth Remains Resilient

The de-Americanization thesis requires U.S. growth to falter. But the structural foundations of the American economy are stronger than the narrative suggests.

Our growth index tells the story. Yes, growth impulses softened in Q4 2025. The index dipped below momentum in mid-October and the trend turned bearish, which only added fuel to the de-Americanization fire. But rather than accelerating into collapse, growth stabilized. By early January, the index pushed back above momentum and briefly flipped bullish before settling into neutral territory where it sits today.

The economy absorbed the Liberation Day tariff shock. It digested higher rates. And it kept moving forward. U.S. growth slowed in Q4 and had every opportunity to crater. It didn’t take it. The failure to accelerate into a bearish trend is itself the signal. We think the whipsaw back after months of equity consolidation is nearing.

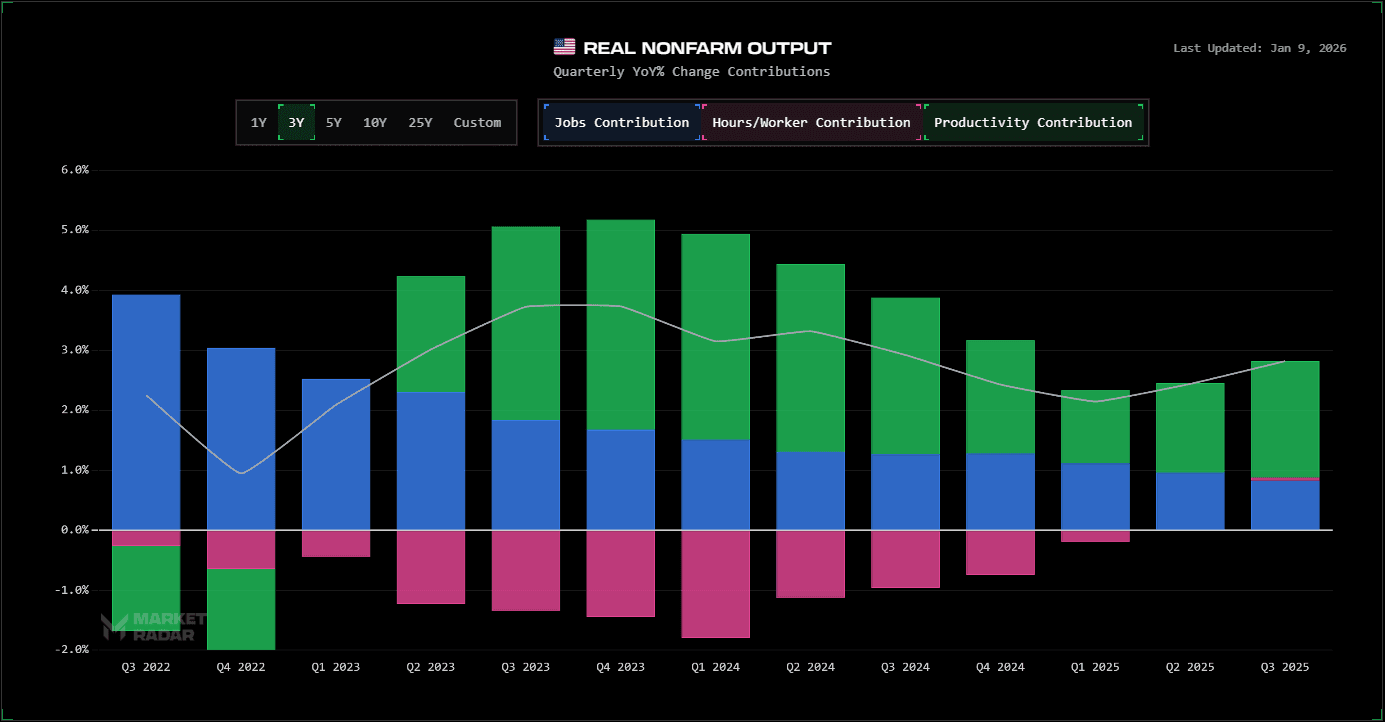

Real GDP continues to grow well above target. Jobless claims refuse to move materially higher. Real nonfarm output continues climbing, with productivity once again expanding after shrinking throughout 2024. Consumer spending alone contributed 2.3 percentage points to growth. This is not an economy on the brink of losing its edge.

And the fiscal dimension that most analysis overlooks remains firmly in America’s favor. The U.S. is running deficits above 6% of GDP, with the One Big Beautiful Bill Act set to deliver $350 billion in additional stimulus by the second half of 2026. Europe’s fiscal rules constrain stimulus even during downturns. Japan has exhausted its room. The U.S. alone has both the willingness and ability to spend through soft patches.

Why Positions Unwind Violently

The crowdedness of the de-Americanization trade creates a vulnerability that transcends fundamentals. When everyone is on one side of the boat, the slightest shift triggers cascading liquidations. Friday provided a textbook demonstration of exactly how this works with gold and silver.

When the Warsh nomination hit, it challenged the consensus view that the Fed would remain accommodative and the dollar would keep weakening. But the price action that followed wasn’t investors calmly reassessing their fundamental views. It was the brutal mechanics of positioning coming undone.

And that’s what’s been happening across the entire metals complex. When you look at the last few months, you see copper declining while gold and silver kept rising. That divergence matters. Copper has significantly more industrial applications. If the metals rally were driven by fundamentals, if it were really about AI-driven data center demand or renewable energy buildout, copper would be leading. Instead, copper lagged while the monetary metals melted higher. The fundamentals weren’t in control. The speculators were. And speculative trades unwind the hardest.

The de-Americanization trade is reflexive. It feeds on itself. Dollar weakness makes EM assets more attractive in dollar terms, which draws inflows from global investors, which supports EM currencies, which makes the dollar weaker still. The trade reinforces itself in a virtuous cycle that feels like fundamental validation but is actually just positioning begetting more positioning. Reflexivity, however, works both ways. If the dollar stabilizes for any reason, the cycle reverses. EM assets become less attractive, triggering outflows, pressuring EM currencies, reinforcing dollar strength. The virtuous cycle becomes vicious.

The Trump 1.0 Playbook

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

We’ve seen this movie before. And we know how it ends.

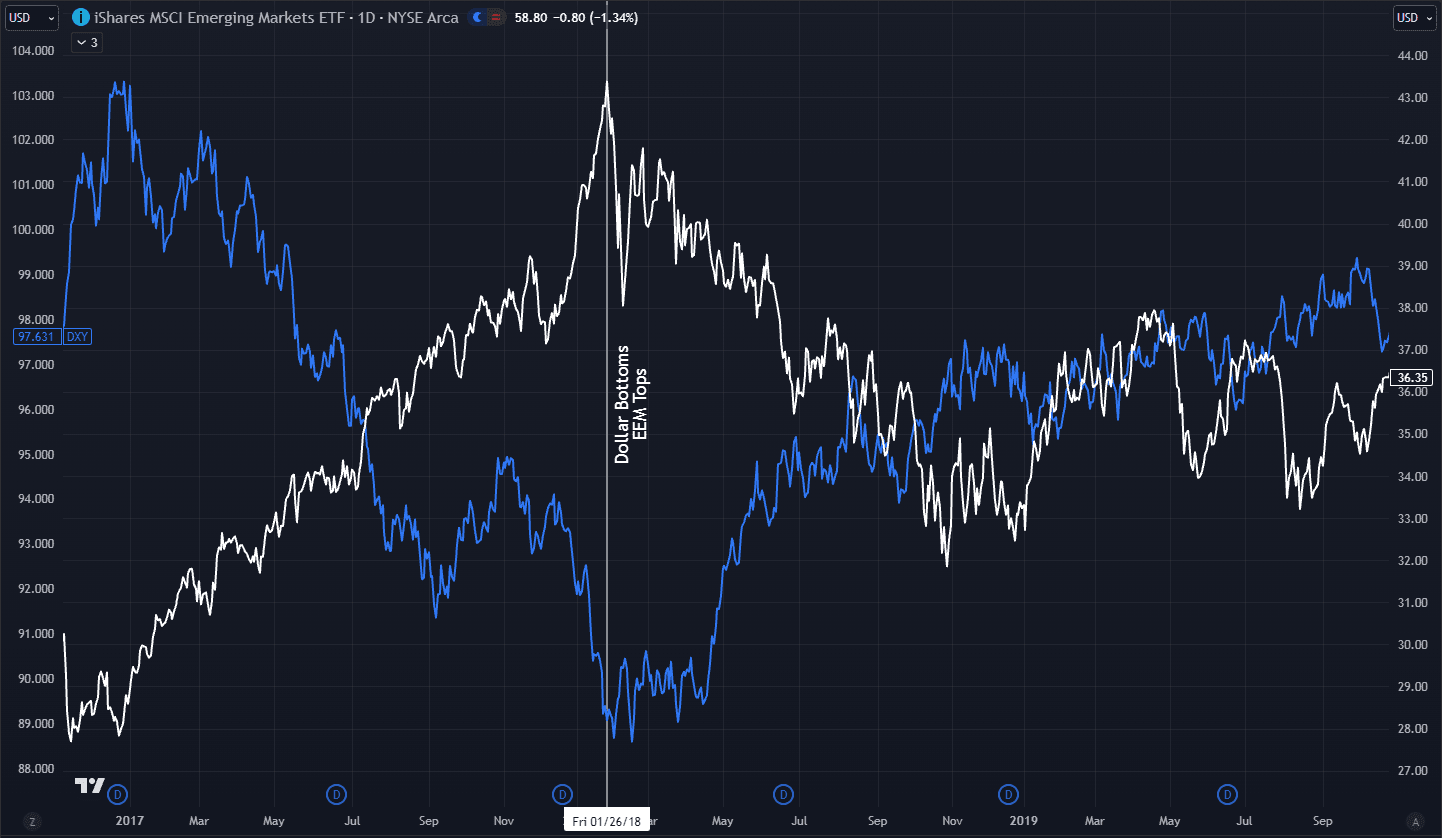

Let’s go back in time to 2017. The dollar was collapsing, posting its worst annual performance in 14 years with a decline of roughly 10%. Emerging markets were the beneficiaries of that weakness, rallying 38% for their best year since 2013. EM currencies broadly appreciated against the dollar. Analysts spoke of a “Goldilocks” environment where everything was falling into place for international assets. Jeffrey Gundlach called for continued EM outperformance. By January 2018, the consensus had become unanimous in a way that should have been a warning sign. Emerging markets were the trade of the decade.

Then the dollar found a floor.

What followed was a violent reversal. Fed tightening cascaded through vulnerable EM economies. Turkey’s lira collapsed. Argentina’s peso suffered its largest one-day drop in three years. By August 2018, EEM had fallen to $41.13, surrendering essentially all its 2017 gains in a matter of months. The generational opportunity turned into a generational trap for anyone who arrived late.

Now consider today. In 2025, the dollar posted its biggest annual decline since when? Since 2017. The magnitude? Roughly 10%. Emerging markets rallied 34%, within striking distance of that 2017 benchmark. Analysts have declared EM bears extinct. Bank of America heralded “the next bull market.” The consensus is unanimous in a way that should feel familiar by now.

The dynamics are identical. The positioning is identical. The narrative is identical. And the administration overseeing it is the same one that watched it all unravel last time.

This is a template that played out under the same political backdrop, with the same tariff-driven volatility, and the same consensus euphoria that we’re watching today. The 2017-2018 cycle didn’t end because EM fundamentals collapsed or because a recession struck. It ended because the dollar stopped falling, and that was enough. When the primary tailwind disappeared, the positions built on that tailwind came undone with remarkable speed.

We’re not predicting a mechanical replay. Markets never repeat exactly. But history provides a useful prior when conditions align this closely. The same trade, the same consensus, the same administration. The burden of proof has shifted. Those betting on continued EM dominance need to explain why this time is different. Because last time, under nearly identical circumstances, the reversal was swift and the losses were real.

The Underappreciated Trade

Here’s what the de-Americanization crowd keeps missing. The S&P 500 is essentially a representation of global growth.

A lot of the world runs on companies that are in the U.S. stock market. If you’re a pension fund manager overseas or a hedge fund manager overseas, to decisively make the decision to not have exposure to the United States stock market is almost saying you don’t want to own a large chunk of the world. To make that bet and persistently win would imply drastic shifts that, at the moment, aren’t plausible to make.

There’s no foreign Google. No foreign Meta. No foreign Apple competitor at scale. American tech dominates in a way that de-Americanization advocates prefer to ignore.

And consider the current setup. Oracle is down 50% from its highs. Microsoft has been struggling. Amazon hasn’t moved. These mega-caps have been sitting out the rally. Yet the Nasdaq keeps making higher lows. Think about what that means. The index has stayed this high for this long without these mega-cap participants. Now imagine what happens if Oracle finds a bottom. If Microsoft catches a bid. These companies can bounce 20-50% and still be in bear trends. But if they do start moving, where do you think the indexes go?

The contrary trade right now is actually U.S. equities. Everyone has been watching the dollar implode and fearing that the U.S. asset trade is coming to an end. But the Nasdaq is quietly setting up for a catch-up move. The AI theme that pushed indexes to all-time highs last year burnt out for a bit. CapEx spending fears caught up. Expectations got stretched, and AI growth couldn’t meet those expectations. The market corrected by chopping around for months rather than crashing.

Now expectations have pulled back enough to catch up with reality. If growth can push through and AI expectations actually materialize into real money, we should head higher from here. The metals theme may be burning out. And if it takes the wind out of that trade, a new theme enters the arena. U.S. equities are that underappreciated theme.

What the Reversal Looks Like

If the de-Americanization trade unwinds, the effects cascade across asset classes in predictable ways.

EM equities underperform because dollar strength mechanically pressures returns for U.S.-based investors. Capital flows reverse as the reflexive cycle shifts into reverse. The generational opportunity narrative fades as investors remember why they were underweight emerging markets in the first place.

Metals correct further. Friday wasn’t a one-day event. It was the beginning of a larger repricing. The fundamentals weren’t driving the rally. Speculators were. And speculative trades unwind the hardest. Gold and silver were the purest expressions of the debasement thesis. If that thesis is losing its grip, metals have substantial downside remaining.

U.S. equities reassert leadership. For all the talk of rotation, American markets remain home to the highest-quality companies, the deepest liquidity, and the most transparent governance anywhere. If the dollar stabilizes and growth holds, capital flows back to where it was always most comfortable.

Timing and Catalysts

We’re not calling for an immediate collapse of EM or a moonshot in the dollar. The thesis is more nuanced. The de-Americanization trade is now a crowded bet with asymmetric risk to the downside, and Friday offered the first real crack in the narrative.

The timing hinges on several factors. Dollar price action matters most. DXY needs to break above mid VAMP at 97.50 first, then clear momo at 99 to confirm a reversal is underway. Until we see that sequence, the dollar remains in a downtrend regardless of the fundamental case. Fed messaging shapes expectations. If Warsh’s confirmation process reinforces hawkish expectations, the dollar bid strengthens. Growth data can shift sentiment. Any upside surprises in U.S. GDP, productivity, or employment challenge the fading America thesis.

Our System currently reads an Inflation regime with Risk-On dynamics, but growth strength sits at neutral levels. We’re on the border between a slowdown and risk-on, with inflation impulses quite strong but growth not yet firmly bullish. The setup is fragile enough that a shift back toward Slowdown or even Risk-Off isn’t far away. We’ll let the regime signals guide positioning. But the macro backdrop increasingly favors American assets over the crowded alternatives.

Why This Matters

The danger of consensus trades isn’t that they’re wrong. It’s that they’re crowded. And crowded trades unwind violently when the narrative breaks.

The de-Americanization thesis may ultimately prove correct over a multi-decade horizon. The arc of history may indeed bend away from American dominance. But over the next six to twelve months, we think the risk-reward has flipped.

Everyone is positioned for dollar weakness, EM outperformance, and Treasury abandonment. Friday showed what happens when that positioning meets an unexpected shock. We don’t think Friday was an anomaly. We think it was a warning.

The world isn’t leaving America. It’s about to remember why it was there in the first place.