13 MIN READ·MAY 18, 2026

Two economies, One Market

MR

CO-FOUNDER · MARKET RADAR

You've seen the argument a hundred times by now. The stock market is one thing, the economy is another, one of them has to be lying. Sentiment is in the gutter, the consumer keeps showing strain, the indices keep grinding higher, and something is supposed to give. The frame is wrong. The stock market is the economy. They're the same object from different angles. The split people are reacting to is real, they're just describing it wrong. The real divide runs between enterprises and consumers, and this cycle is being driven by something we haven't really seen before.

Enterprises are stimulating the business cycle. Themselves. With their own balance sheets. At a scale large enough to move GDP. Fiscal is doing its part, running deficits near 6% of GDP, well above average. But the Fed is offsetting most of that impulse through the rate channel. Net the two against each other, and what's left moving the needle is the corporate sector. And it only reaches people inside the loop. That's been the trade since late 2022. The gap is wider today than at any point in the cycle. And our System just registered the first crack on the aggregate growth side last week, which we'll get into in the member section.

Where the Stimulus is Coming From

Stimulus normally comes from two places. The Fed cuts rates and makes borrowing cheaper for everyone. Or the government spends money it doesn't have and pushes it into households and contractors through programs and checks. Both pull demand forward, just through different doors. The second one is happening hard right now. The federal deficit ran 5.8% of GDP in fiscal 2025 and is projected to clear 6.8% in fiscal 2026, against a 50-year average of 3.8%. That's a number you'd normally only see in a recession or a war. And the trajectory keeps widening. But the Fed is running directly against it. The 30-year is at 5.1%. Polymarket hike odds are at 31%. The cutting cycle is officially over, and Warsh just walked into a forward curve pricing hikes through mid-2027 against the Fed's own 3.125% terminal estimate. Whatever fiscal is pumping in, the rate channel drains out at roughly the same pace. The two cancel. The household side, which responds most directly to both, gets almost none of the net impulse.

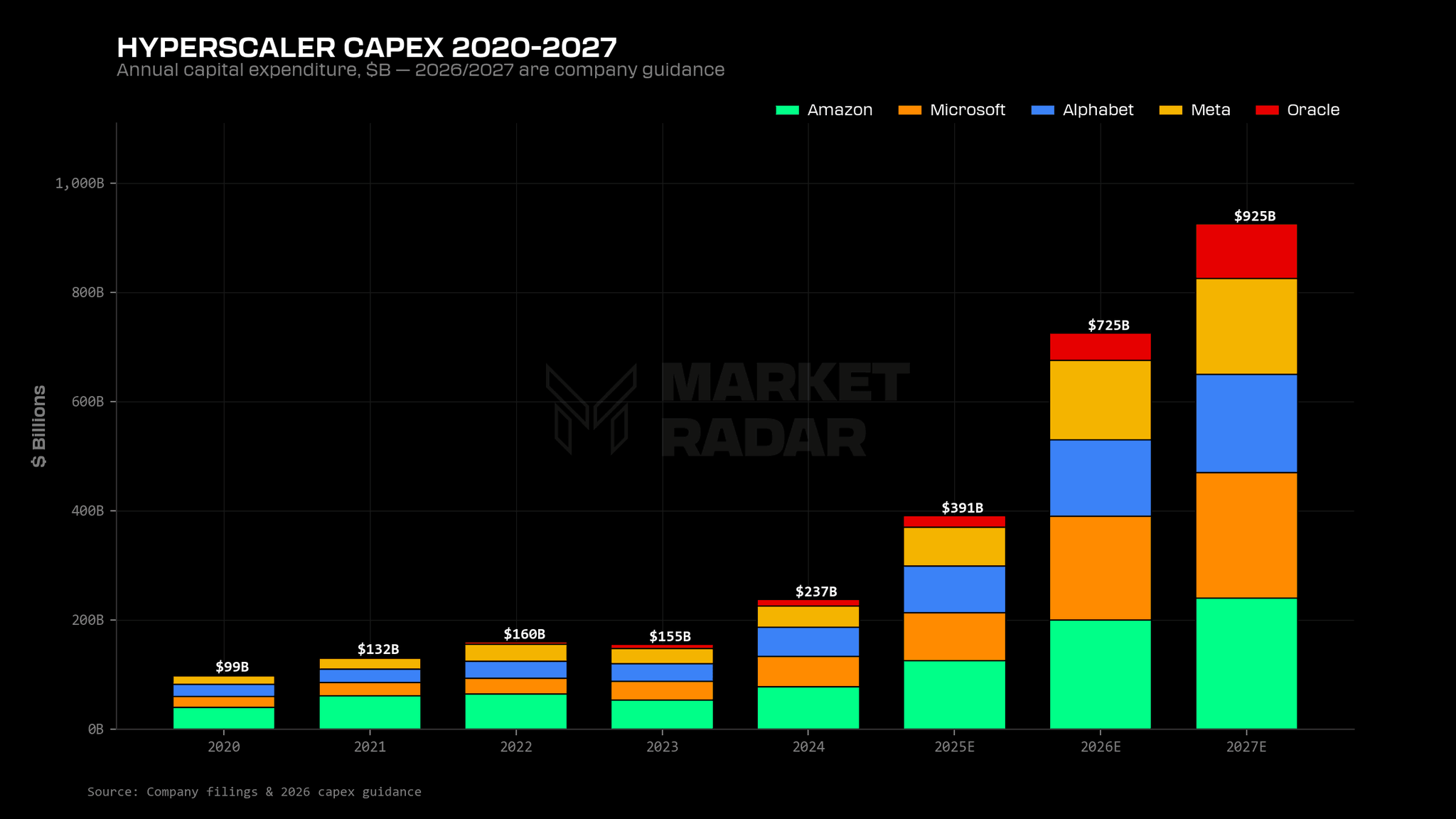

What's left moving GDP is private capex. Specifically the hyperscalers. Amazon, Microsoft, Alphabet, Meta, and Oracle have collectively committed $725-800 billion of capex in 2026, with Microsoft alone at $190 billion and Amazon at $200 billion. The combined number clears $1 trillion in 2027. None of these are typos.

For scale, look at the last time we did something like this. The telecom boom in the late 1990s peaked at roughly $135 billion of annual capex in 2000 dollars, around $213 billion in today's money. Total cumulative investment from 1996 through 2001 came to about $500 billion. The hyperscalers are now spending about 3.5 times the inflation-adjusted peak of that buildout. Every year. And the trajectory is still climbing. Goldman estimates data center construction alone added 0.2% to GDP growth in 2025. That's just the buildings. Add in the chips, the networking gear, the power infrastructure, and the second-order spend at the suppliers' suppliers, and tech capex contributed 2.28 percentage points to first-half 2025 GDP growth. More than consumer spending. That's the first time tech capex has outrun the consumer as the largest driver of US growth in modern memory.

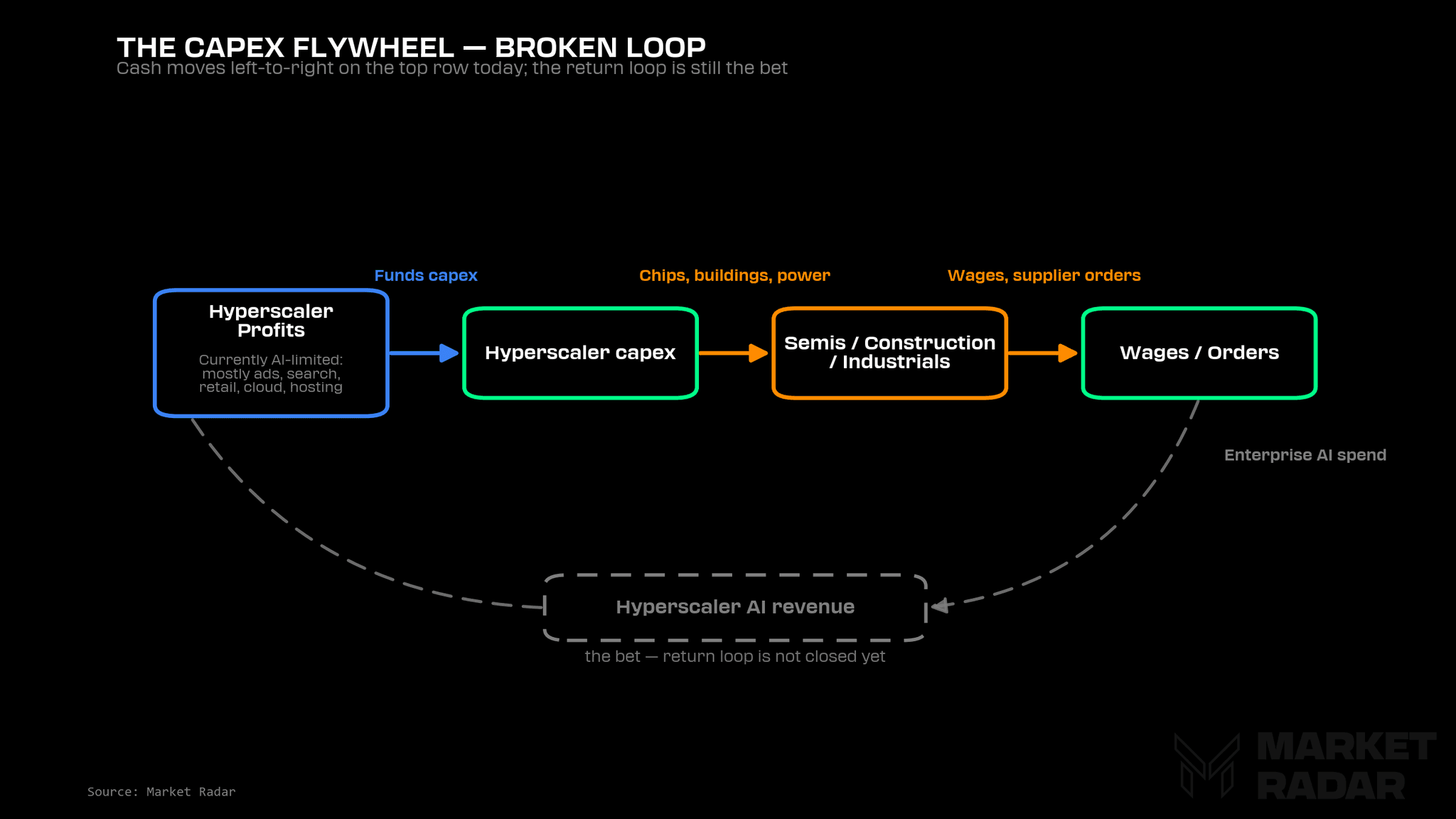

The capex moves real dollars in a specific pattern. Hyperscalers spend on compute and infrastructure. Compute makers and construction firms print extraordinary numbers off that spending. They pass the wealth downstream to industrial suppliers, to the trades, to the regional economies where the data centers are getting built. The hyperscalers underwrite the whole chain on a bet that AI revenue eventually flows back to them in a form larger than what they sent out. Every link inside the loop benefits while the loop is spinning. The consumer is not inside the loop.

What "Inside the Loop" Actually Means

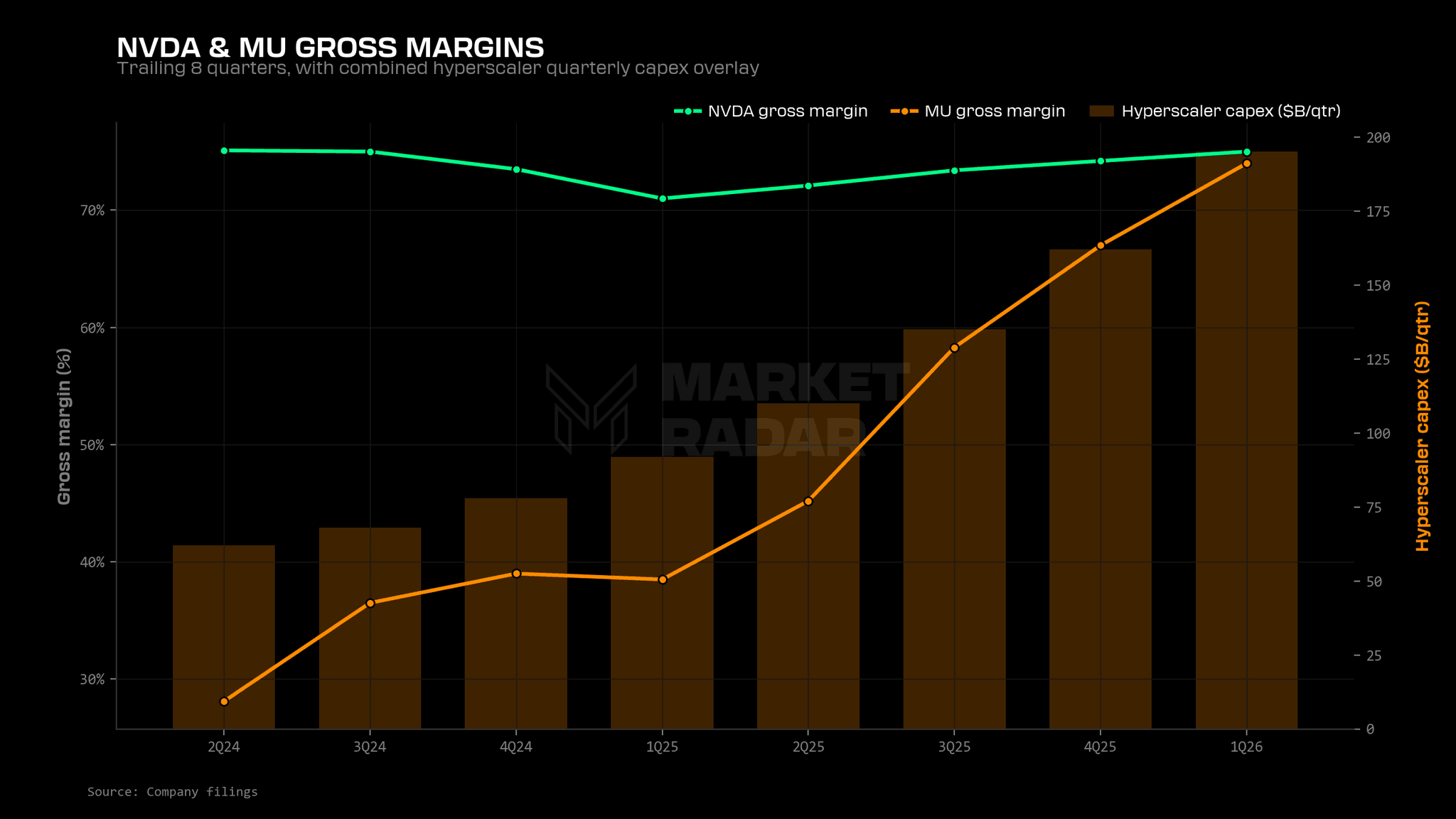

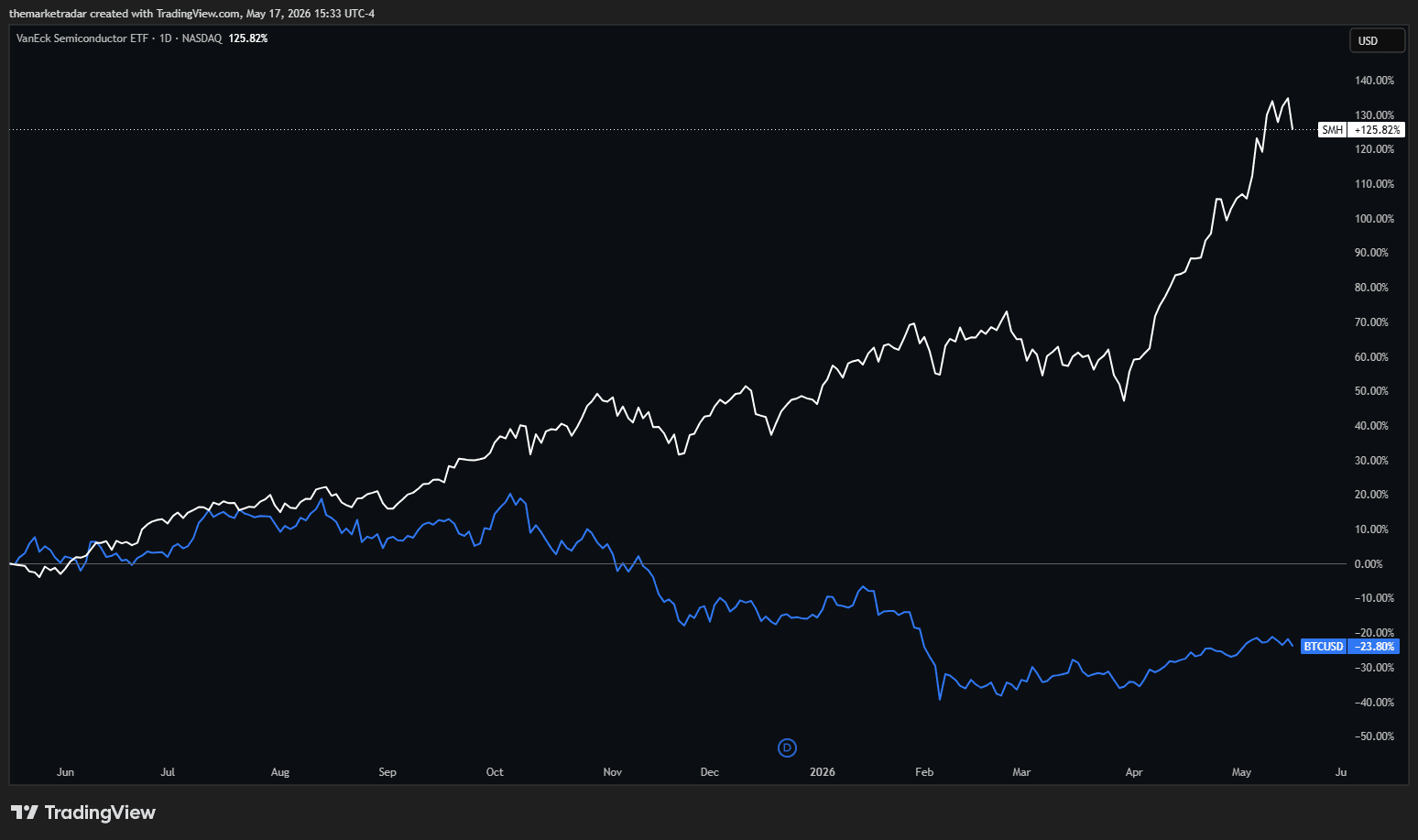

Easiest place to see the loop is at the receivers. Nvidia closed fiscal 2026 with a 63% net margin and a 75% gross margin on $68 billion of quarterly revenue. $43 billion of net income in a single quarter. Micron just put up 74% gross margins on $24 billion of quarterly revenue, three times last year's number, at double the margin. AMD and Broadcom are in the same neighborhood. These aren't normal numbers for a hardware business. Hardware businesses normally compete with each other for fixed customer budgets. These businesses are competing for whose order book gets filled first, and the customer base is racing them to overspend. SMH is up 54% year to date. It's up 125% over the past twelve months. That's what a basket of monopolistic suppliers looks like when their customer base has agreed to overpay them for two years straight.

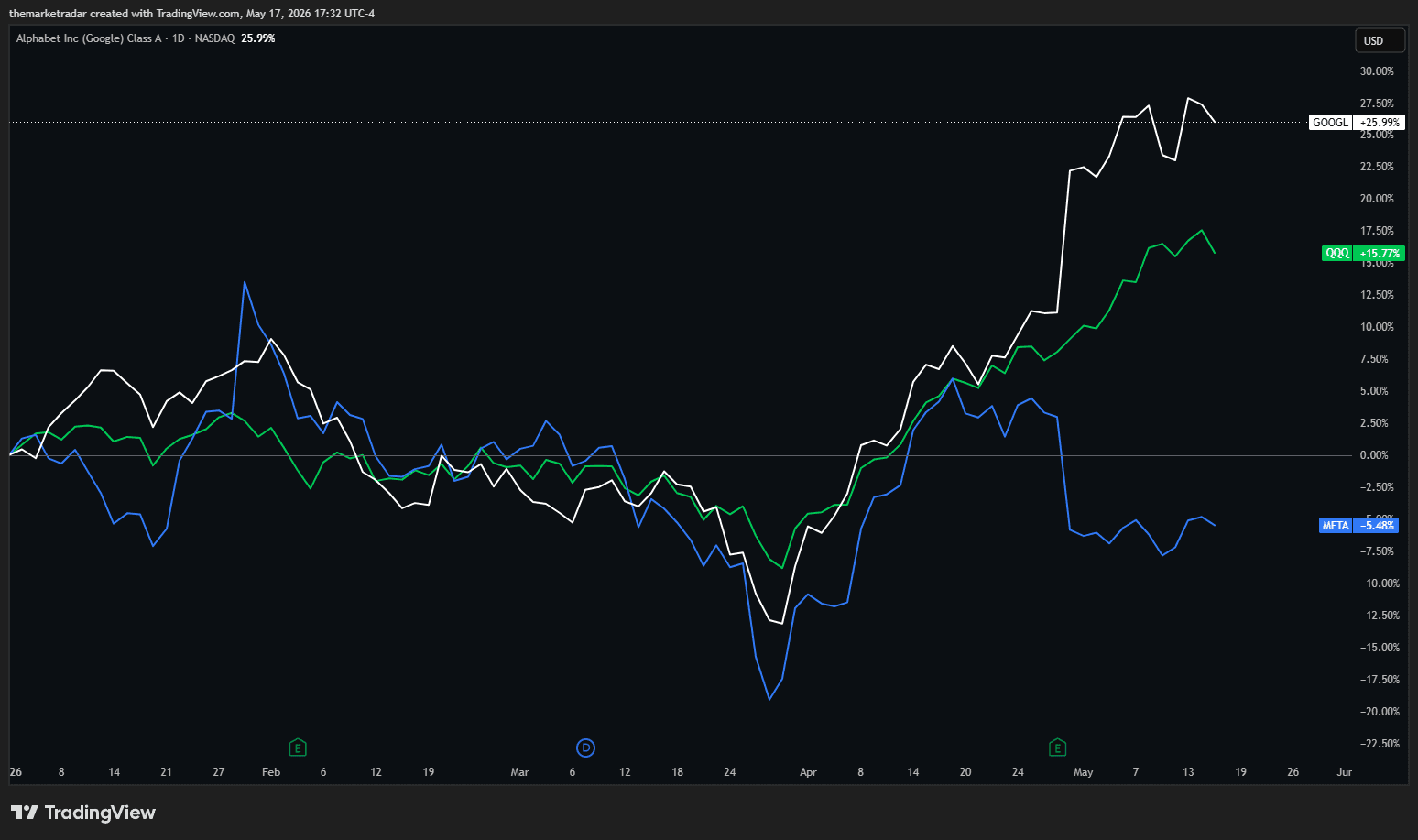

The more interesting story is one layer up, at the hyperscalers themselves. Not all of them are getting the same treatment, and the difference tells us something important about how the loop works. Meta and Alphabet make the cleanest comparison. Both spending north of $135 billion this year on the same kind of stuff. The stocks look completely different. Meta is down 6% year to date, more than 20 points behind the Nasdaq, with FCF compressing hard as capex ramps. Alphabet is up 28%, with its cloud business running its hottest growth rate in years.

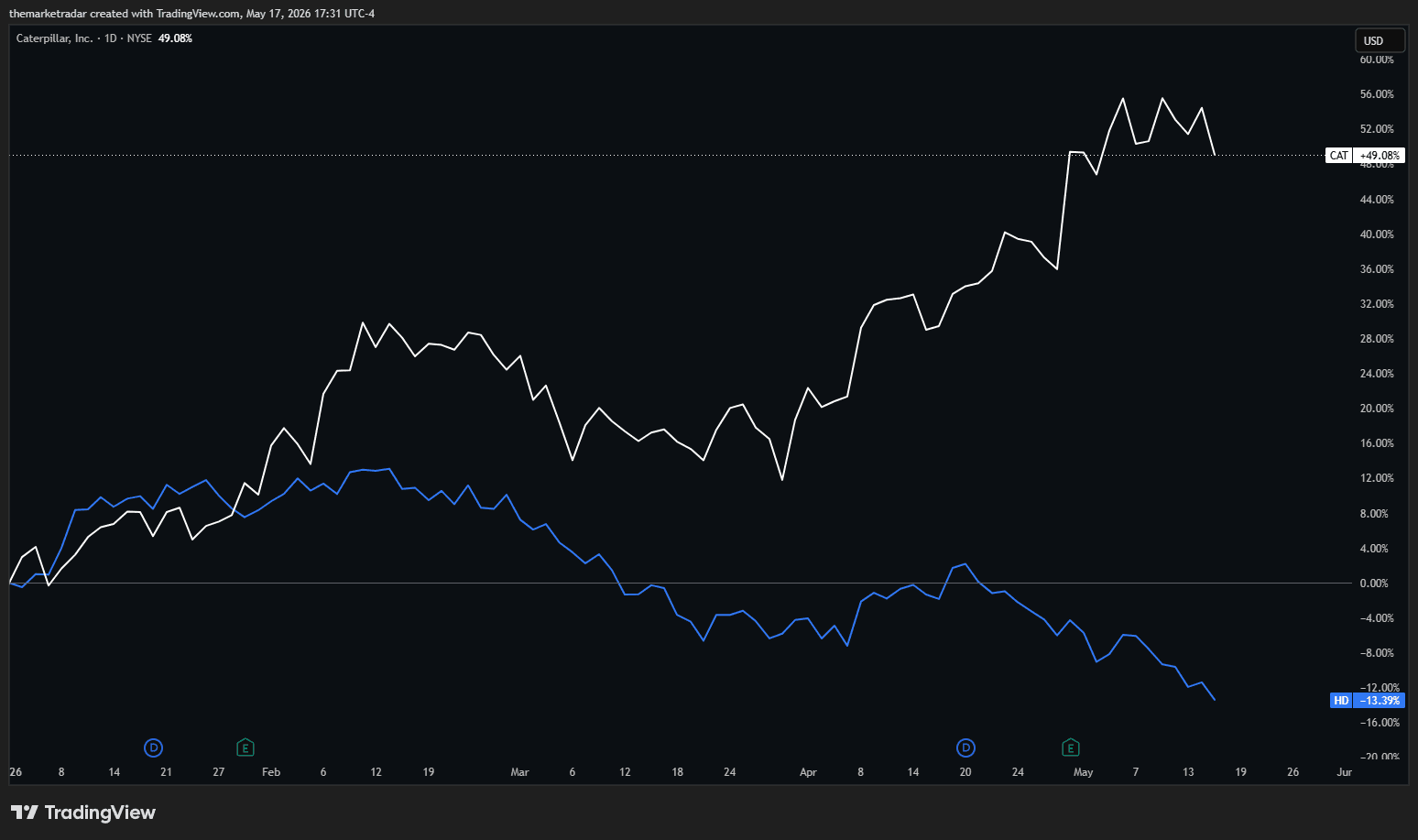

The difference is structural because Alphabet built TPUs over a decade ago. It's the only hyperscaler that runs a fully internal accelerator stack at scale. When Alphabet spends, a chunk of the flow stays inside the company. Its silicon program catches some, its cloud business catches the rest. And Alphabet is selling TPU capacity to Anthropic and OpenAI today, with Meta reportedly next. Every external TPU dollar is a stimulus dollar that left Alphabet's capex line and comes back as Google Cloud revenue. Alphabet is on both sides of the loop. It spends like a hyperscaler and it collects like a receiver. Meta doesn't have that. Its chip program is years behind, and most of its capex flows out to Nvidia, Broadcom, and inference rental partners. Every dollar Meta spends is a dollar leaving its income statement and landing somewhere else. The market sees the difference. Inside the loop, you get paid for keeping your own flow. Export it, and the market treats you like the receivers are eating your lunch. Same thing in industrials. Caterpillar is participating in the buildout. It holds up. Home Depot doesn't participate. It breaks down. Same sector, same labor pool, same equipment. Two completely different stock charts attached to which side of the loop each name feeds.

What "Outside the Loop" Actually Means

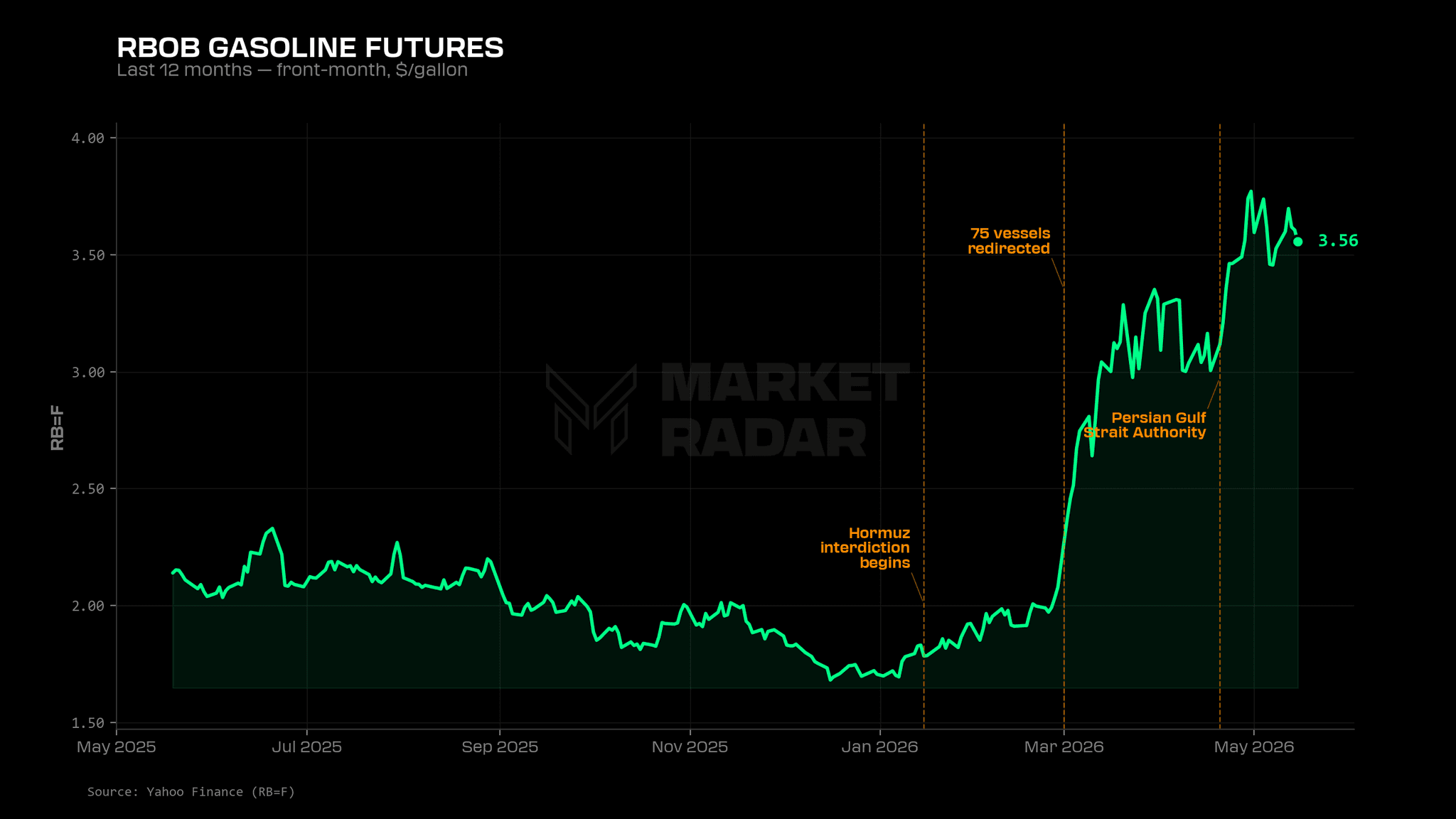

The consumer is on the other side of the same economy. They get every cost the enterprise stimulus produces, with none of the offsetting benefits. Starting with energy, RBOB gasoline has more than doubled since January, from $1.70 to $3.55, and Brent is sitting above $100 with the Strait of Hormuz under active interdiction. The Iran situation we covered in The Stagflation Threshold hasn't resolved: 75 commercial vessels redirected, Iran's formalized a Persian Gulf Strait Authority, the Aramco CEO is now pricing June closure as a base case rather than a tail. The downstream is showing up everywhere: fuel costs flagged across all twelve Fed districts in the Beige Book, jet fuel doubled through Q1, anything touching freight or distribution getting squeezed alongside it.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Layer on rates. The 30-year is at 5.1%, a level we haven't seen since before the financial crisis. Polymarket hike odds are at 31%. The cutting cycle is over. Powell is out, Warsh is in, and he's inherited a forward curve pricing hikes through mid-2027 against the Fed's own 3.125% terminal estimate. For a household, that means mortgages that won't budge, auto financing that stays expensive, and credit card APRs piling on top of the energy tax. The escape valve the Fed has provided in every prior consumer-stress cycle is sealed shut.

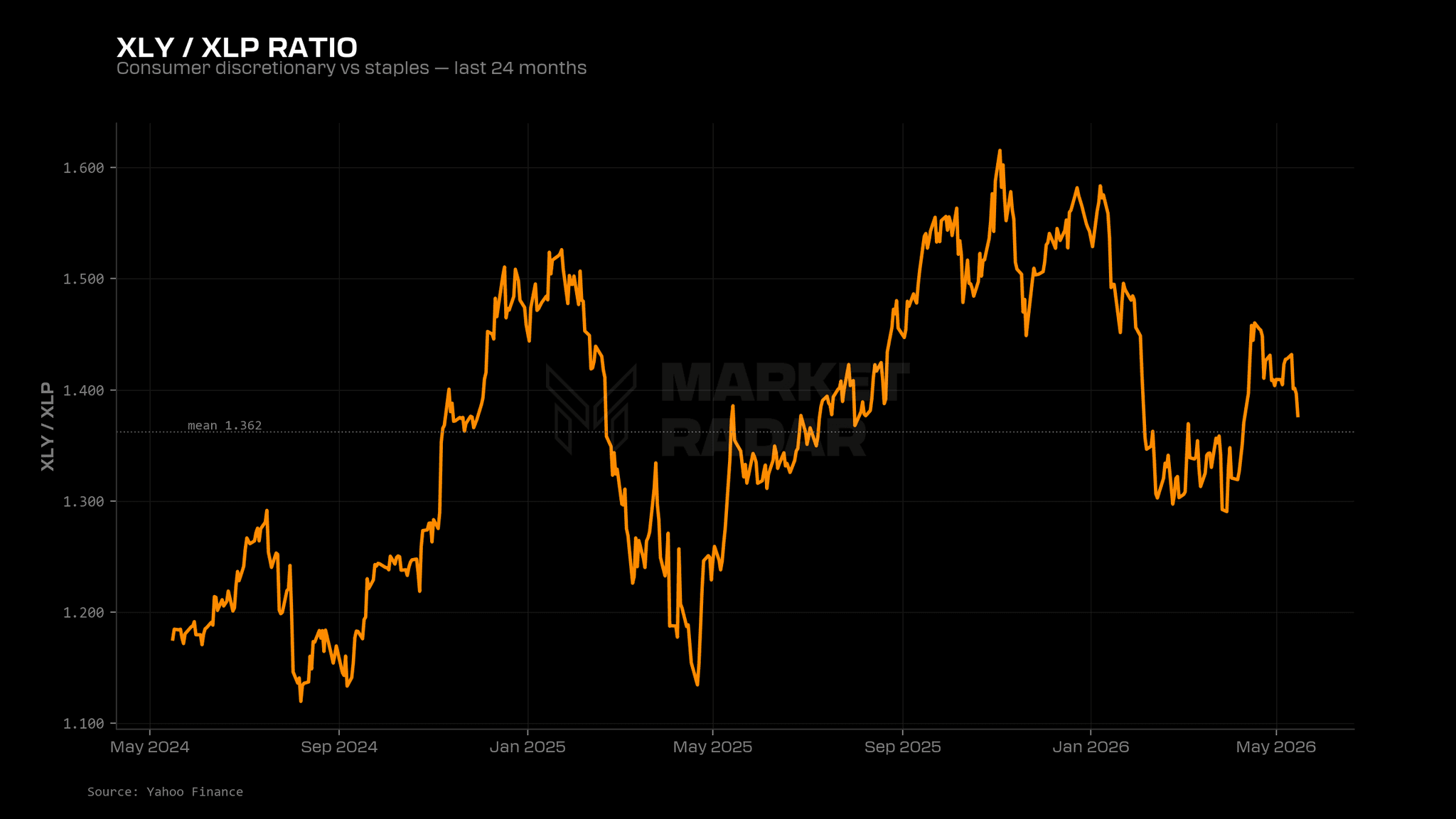

The enterprise stimulus is part of why inflation has stayed hot enough to keep the Fed pinned. Hyperscalers are consuming real industrial inputs at scale, bidding up wages in skilled trades, and adding aggregate demand at exactly the moment the Fed would normally be cutting to help the consumer. The same circuit that's stimulating the corporate sector is also blocking the household from getting any relief on rates. Inside the loop, that's a feature. Outside the loop, it's a vise. The names exposed to this side of the economy are printing the chart you'd expect. Nike, garbage. Lululemon, cooked. Home Depot, breaking down. Consumer discretionary as a sector has been chopping sideways for over a year. These companies don't have a path into the flywheel. They don't sell shovels to data centers. They sell to a consumer who's been asked to absorb a permanent energy shock and a frozen rate curve at the same time, with no offsetting stimulus reaching them.

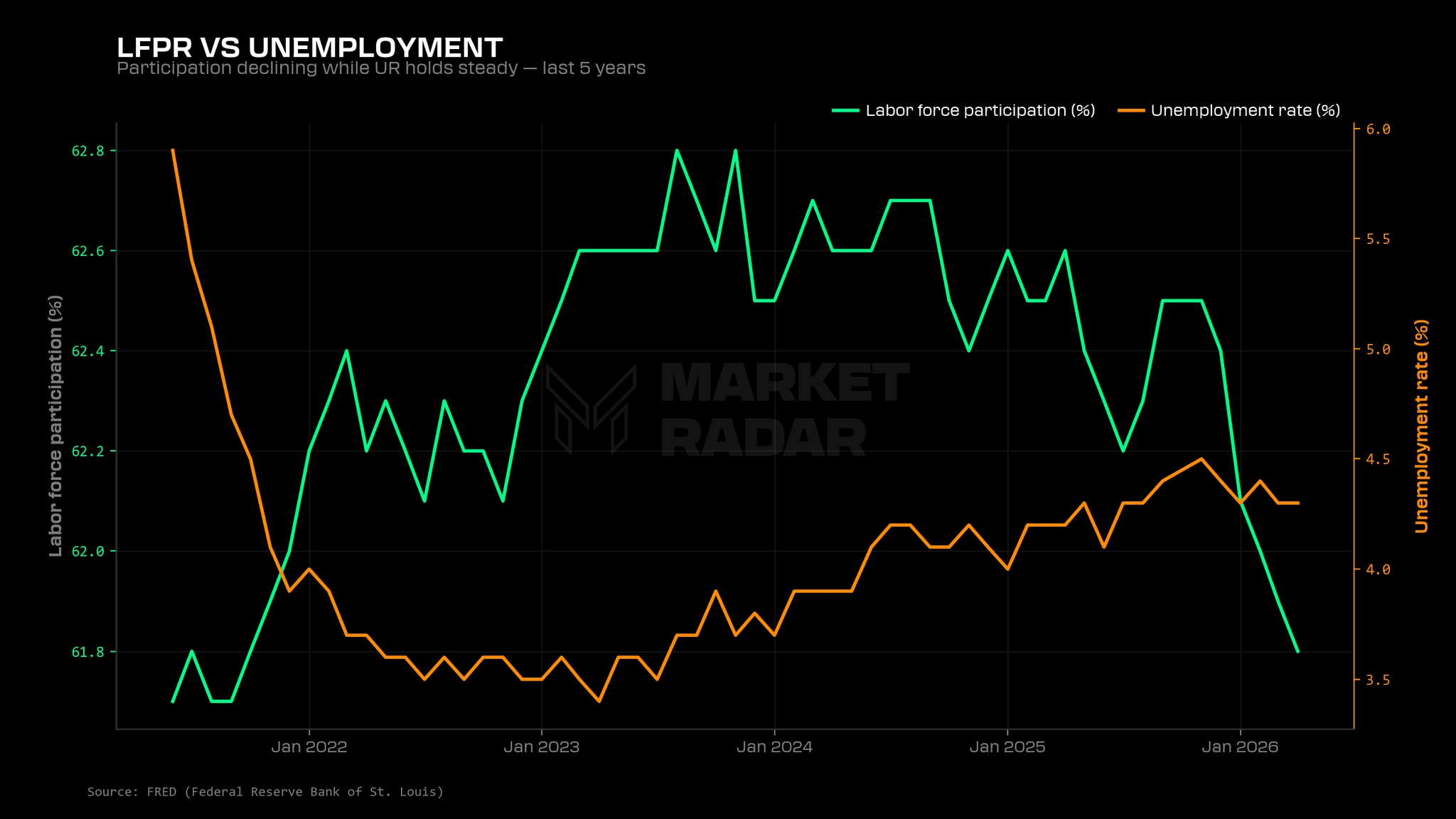

The labor market shows the same thing. Headline unemployment is steady at 4.3%, but the stability hides what's underneath. People aren't finding jobs, they're leaving the labor force. Participation just hit 61.8%, a multi-year low. The workers still in the game can't move either. Quits rate at 2.0%. The job-switching wage premium just collapsed from 5.0% to 3.8% in a single month. Workers are stuck. Except inside the loop. A skilled tradesperson who pivots into data center work gets a 25-30% raise. The median worker who switches anywhere else gets 3.8%. Same bifurcation, different proof.

The Bitcoin Tell

Bitcoin deserves its own section. The bitcoin chart is the cleanest single piece of evidence we have that the loop is closed. Over the last year, semiconductors are up 125%. Bitcoin is down 23%. Similar risk profile, same regime, same headlines. Risk-On reading from our System for months on end. And they're pointing in completely opposite directions.

We wrote about this in The Imminent Rise of Bitcoin a couple weeks ago. Astraeus has been sidelined since we sold at $115k in October. Bitcoin has been grinding sideways and lower while every other risk asset pushed higher. Consensus take is that the cycle is broken. ETFs changed the structure. Supercycle theory is dead. We disagree, and the reason we disagree is exactly the dynamic this ledger is about. Bitcoin runs on retail. The entire history of the asset says so. Every prior bull market was powered by households with extra cash overflowing past stocks and out into the high-vol end of the risk curve. Bitcoin sits at the far end of that curve. No dividend, no cash flow, no central bank backstop. The only thing that catches a bid is excess. When the consumer has spare cash and stocks are already bought, the next dollar gets adventurous and goes hunting. That's when bitcoin moves.

We don't have that today. The flywheel powering semis and the leaders is institutional. It's self-sufficient. It doesn't need retail. Hyperscalers don't need the consumer to grow to fund the loop. They need ad budgets, cloud contracts, and subscription revenue to hold their level, and those behave like staples as long as the business cycle doesn't actually turn. Sentiment in the gutter doesn't break that. A real contraction would. Receivers don't need the consumer to print margins either. Their customer is the hyperscaler, not the household. And none of the dollars circulating inside the loop ever overflow far enough out the curve to land in bitcoin. The asset that screams when households have spare cash is silent, because households don't have spare cash. Bitcoin lagging through a Risk-On year is the cleanest read we have on what's actually going on. The tape looks like Risk-On on paper. Underneath, it's enterprise stimulus carrying the whole thing with the Risk-On label borrowed from prior cycles. The flip side matters too. The day bitcoin starts to participate is the day the loop has finally pulled the consumer in. Until then, SMH at +54% and BTC at -19% tells us with zero ambiguity which trade has been working and which one is waiting on a setup that hasn't shown up. Astraeus is built to catch that change when it comes. It won't chase it.

Why This Has Held

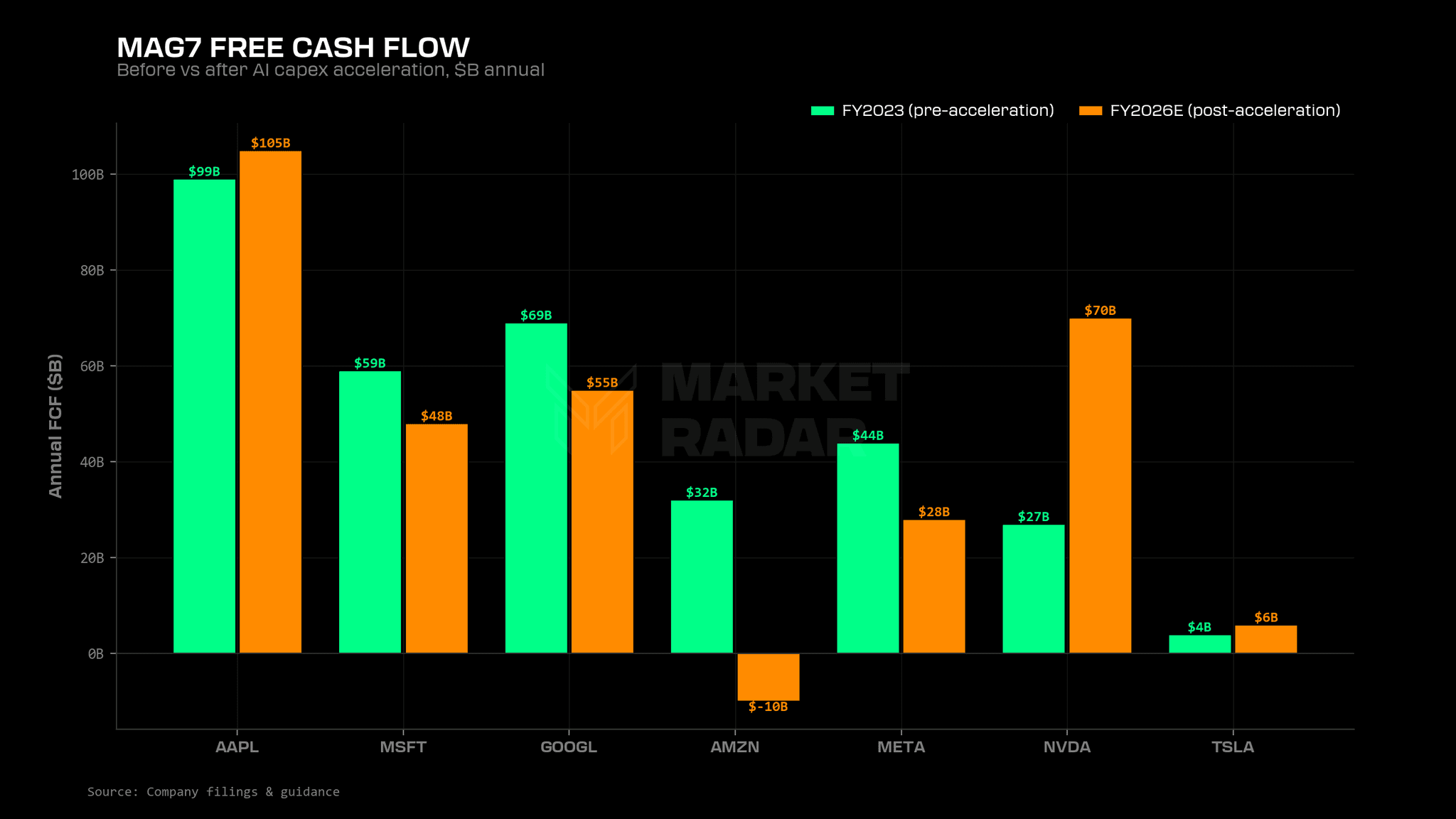

Most people look at this setup and assume it can't last. A market running on enterprise stimulus while the consumer side falls apart feels unstable. Fair instinct. Wrong, so far. Worth understanding why before assuming it's about to break. Hyperscalers have consumer-staple revenue streams in their core businesses. Ad inventory, cloud contracts, enterprise subscriptions, reserved capacity. The cash flows are diversified enough and the moats deep enough that the odds of any of them suddenly not being able to fund capex are about zero. Free cash flow is collapsing across the board. Amazon is on track for negative FCF this year. Meta just raised 2026 capex guidance to $145 billion and halted Q2 buybacks to fund it. But the operating businesses aren't breaking. The cash is leaving as fast as it comes in, by choice, because the boards decided AI position matters more than near-term returns. That's a totally different problem than not having the cash in the first place.

The receivers are insulated too. Order books at Nvidia, Micron, AMD, and the data center construction firms are booked out into 2027. Margins at 60-75% give them enormous absorption capacity for near-term softness. The names inside the loop have revenue visibility the consumer-facing names can only dream about. And the macro indicators have held The flywheel was generating enough top-line stimulus to keep the aggregate growth picture intact even as the consumer-side data was weakening underneath. That's why fading the AI side of the tape without a System signal has been the costliest mistake of the cycle. The trade has been working because the closed-loop structure was designed to work without the consumer. The trade keeps working until either the loop slows down or the consumer-side weakness drags the aggregate growth picture down with it. We just got our first read on which of those happens first.

The Outlook

The current trade is concentrated. Tech, specifically compute, is outrunning everything else. SMH up 54% YTD. The receivers printing at 60-75% margins. The rest of the market chopping sideways. That concentration keeps working as long as the flywheel is spinning. It also concentrates the market's vulnerabilities into the same names. Compute margins will eventually decay. Competition catches up to demand. The easy monopoly returns at the receivers get reset. That's the long-term gravity on the trade. But the buildout is a multi-year plan still in motion, and the receivers hold their position through a lot of it. The decay shows up gradually, in forward capex guidance from the buyers and in margin compression on the seller side. The day any of the major hyperscalers softens its forward capex outlook, those margins start re-rating. That trigger lives on a quarterly earnings timeline. Could be next quarter. Could be the one after.

What people want to do with this setup is reach for the dot-com analogy. Semis look parabolic. Hyperscalers are spending like maniacs. End of cycle is near. We don't buy it. NVDA trades at roughly 30x earnings today, with order books booked into 2027 and revenue growth still running above 70%. Cisco in 2000 traded at 130x selling into leveraged carriers building speculative networks they couldn't fund. The fragility looks completely different. A 2000-style unwind is the wrong base case. What's more likely is a bubble with transitions. The AI buildout keeps moving past compute. The theme everyone is running right now, getting AI out of chatbots and into the real world, implies the next concentration after semis is somewhere else. Robotics, Industrial automation, Physical AI applications. The capital currently feeding compute rotates into the next layer of suppliers without the flywheel itself stopping. Each transition is its own concentrated trade. The bubble migrates across layers.

That has direct implications for how this plays out. The market is hyper-sensitive to enterprise stimulus. Periods of weakness on the enterprise side will send us into Risk-Off windows. Those windows tend to recover within the AI theme. A recessionary style unwind needs the flywheel itself to break, and that requires more than we've seen. The flywheel only actually dies if three things happen together. Compute saturates and margins reset. No transition layer picks up the slack. And the consumer doesn't rebound to fill the gap. Until that triple threat lines up, the cycle has more chapters to go. The bigger near-term risk is dispersion. Tech can dip aggressively while consumer names stay broken. The gap between them is what defines how violent the tape gets when stimulus stutters. Sector rotations get sharper. Volatility windows get more frequent. That's what to position for. The kind of weakness this setup produces along the way.

That's the framework. The System catches rotations once they show up in the data. We don't need to know which sector takes the baton next. We need to know when the data tells us a rotation has started, and it just did. We rode tech up with leverage, and now our System is telling us it's time to take some profits and trim down our risk, here's how we're trading the next leg:

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access