This Beat Covered Call ETFs

Income investing has entered a new era. Traditional sources like dividends and bonds no longer dominate the conversation, investors are turning to more dynamic strategies that use covered call option ETF's. But what if I told you there is a better way to capture similar income without giving up the potential for price appreciation?

At this point, you’ve probably heard the term covered calls, and chances are, you’ve even traded a few yourself. There’s something oddly satisfying about using the options market to squeeze a little extra income out of stocks you already own. It feels efficient, even clever, like you’re capturing value from every angle while the rest of the market waits for price appreciation.

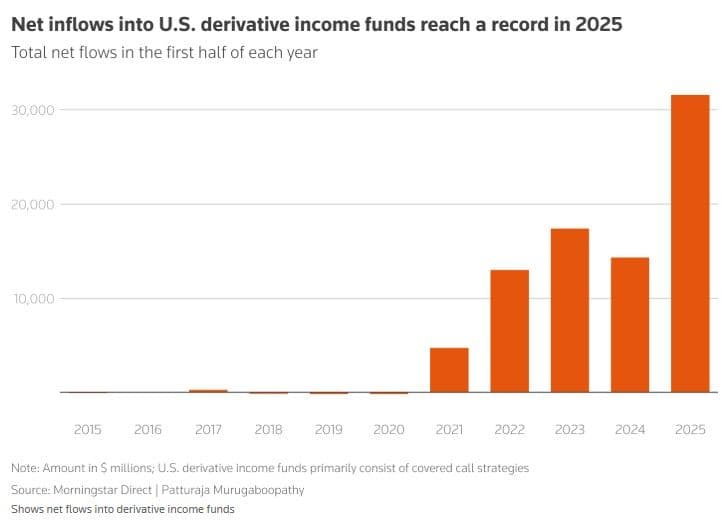

That instinct has gone mainstream. Over the past few years, investors have piled into income-focused ETFs built around covered call strategies. What started as a professional’s tactic for enhancing returns has turned into one of the fastest-growing segments of the entire ETF industry. The promise is simple: generate consistent income while staying invested in equities. For investors weary of market volatility and uncertain rates, it’s an appealing trade.

But the sheer scale of this movement is what’s truly remarkable. The demand for income products has exploded, with covered call ETFs leading the charge and attracting billions in new assets. They’ve become the face of a market obsessed with yield, a symbol of how investor psychology has shifted from chasing growth to chasing income.

And yet, behind this boom lies a quiet problem. The same structure that makes covered call strategies look safe and productive in sideways markets can also hold investors back when markets recover. As we’ll see, the tradeoff between steady income and capped upside is far more limiting than many realize, and it’s paving the way for a smarter alternative in the next generation of income ETFs. We're going to explore why we think there is a superior product to covered calls if you're trying to generate income, and exactly how we use it alongside our strategies.

The Downside Of Covered Call ETFs

The surge in covered call ETFs has been driven by their promise of dependable income and equity exposure, but the structure of these funds comes with tradeoffs that are often overlooked. While they can generate attractive yields in the short run, their long-term mechanics tend to limit both performance and flexibility.

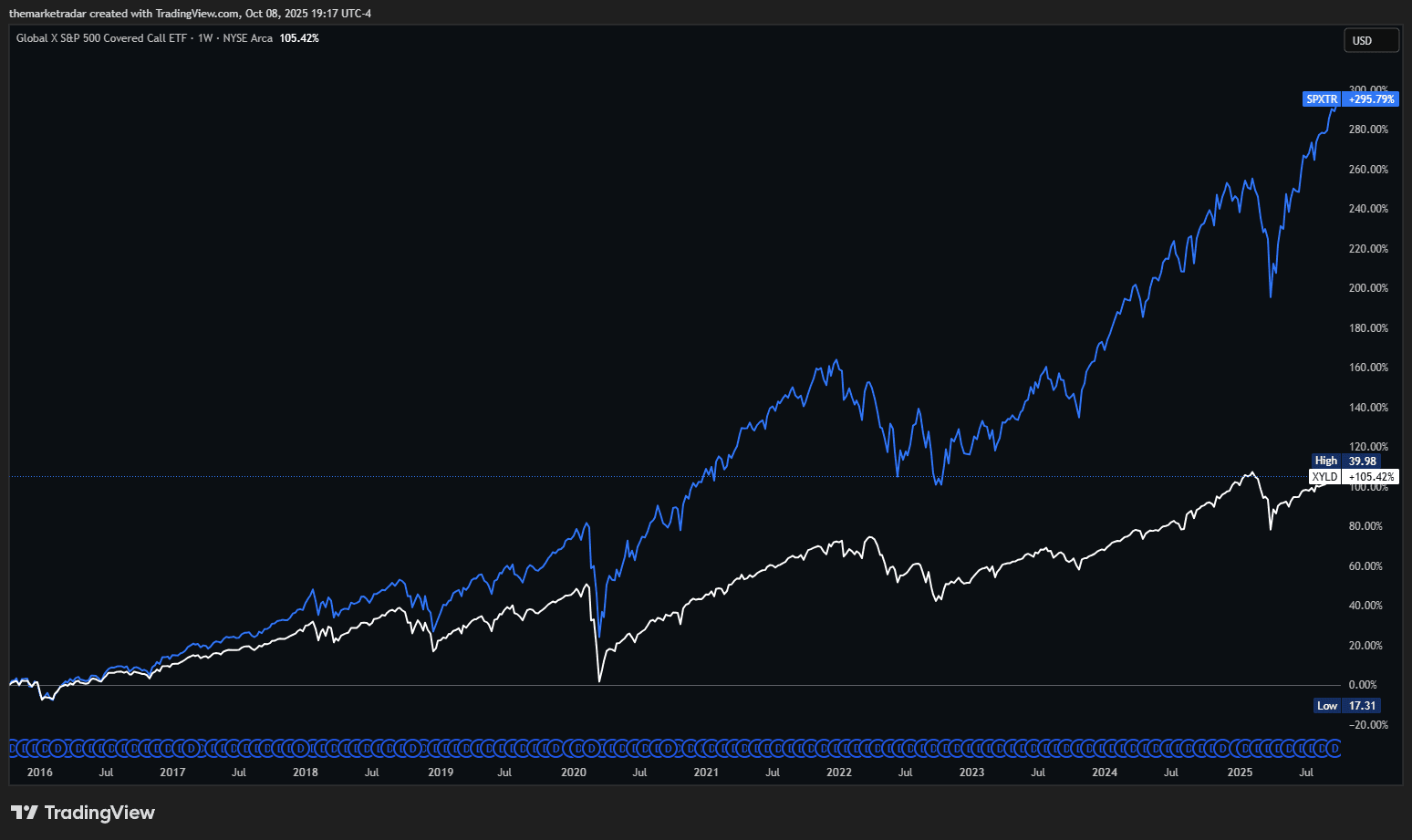

Covered call ETFs sacrifice potential growth whenever markets rally. By selling call options, these funds agree to sell their underlying holdings if prices rise beyond a certain level. That means they collect income from option premiums but miss out on the full upside when stocks rebound. Over time, this tradeoff can cause them to lag far behind equity benchmarks.

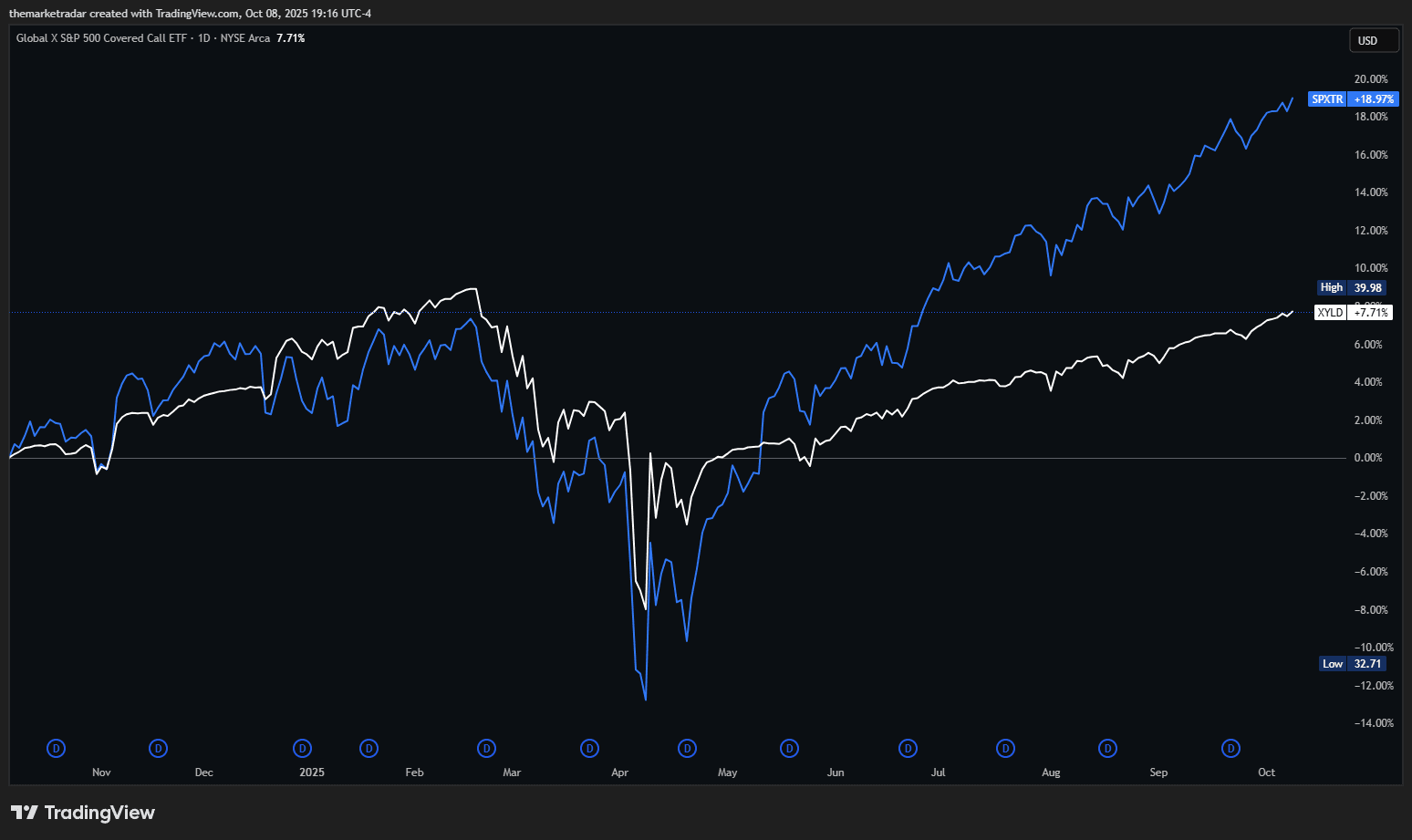

The problem is compounded by how these funds behave during market drawdowns. Because covered call ETFs must stay invested in their underlying index to write new options continuously, they tend to fall just as much as the assets they track. The income from selling calls provides only a small cushion, often just a few percentage points, leaving investors exposed to nearly the same losses as owning the index outright. Then, as markets recover, the ETFs immediately start selling new calls into that rebound. Those options cap future gains, causing the strategy to lag just as prices start moving higher again.

The example below illustrates these dynamics by showing how sensitive these covered call ETFs are to drawdowns in the underlying index, and how they struggle to recover, leading to long-term underperformance against the benchmark, even after accounting for the dividends from the premium collected in the covered call ETFs.

This pattern creates a frustrating dynamic. Covered call ETFs feel safe because they produce steady income, but they rarely protect investors when it matters most. The funds endure most of the downside and then give up much of the recovery, turning what seems like a balanced income strategy into a long-term performance drag.

The Alternative: Structured-Note ETFs & CAIE

Our view is that covered call strategies are better deployed tactically and manually, rather than systematically through ETFs. Still, one income strategy we like, which pays roughly on par with many covered call funds, now has an ETF wrapper that allows investors to participate passively in a more flexible and structured approach. That product is CAIE from Calamos. Before I continue, I'd like to note that we aren't sponsored or affiliated with this issuer. They make a decent product that has caught our attention.

What is CAIE?

CAIE, the Calamos Autocallable Income ETF, launched in June 2025, aims to deliver high monthly income linked to equity market performance while offering built-in downside buffers. It does this through a portfolio of autocallable structured notes, a type of income-producing security that behaves differently from traditional stocks or bonds. We explain it in a podcast here.

What are autocallables?

Autocallables are notes whose income and lifespan depend on how an underlying index performs. Each note pays a coupon (similar to an interest payment) as long as the index stays above a certain threshold called the coupon barrier. If the index drops below that barrier, the coupon for that period is skipped, but the note remains active.

Autocallables also include a protection barrier, typically set deeper below the starting index level. This barrier defines the level at which the principal becomes at risk at maturity. In CAIE’s design, both the coupon and protection barriers are set 40 percent below the initial index level. As long as the reference index stays above those thresholds, investors continue receiving coupons and can expect their principal back at maturity.

Why “autocallable”?

These notes include a feature that lets them end early when markets are performing well. After an initial non-call period (typically one year), the note checks the index level on set observation dates. If the index is at or above its starting level, the note is automatically “called,” meaning it closes out early and returns the investor’s principal along with any coupons that have been paid. If the index is below that level, the note simply continues to the next observation period until it is called or reaches its final observation date over a 5-year term.

In CAIE’s case, the ETF holds dozens of these notes, each with its own observation calendar. Some may be called early, locking in gains and freeing up capital to reinvest, while others continue to pay coupons until their next review. The ETF monitors these monthly across its ladder, which keeps income consistent even as individual notes roll off.

What index do these notes track?

CAIE’s autocallables reference the MerQube US Large Cap Vol Advantage Index, a rules-based benchmark linked to U.S. large-cap equities. The index dynamically adjusts its exposure to S&P 500 futures to target a 35 percent volatility level, meaning it increases or decreases its exposure as markets become calmer or more volatile. Although the methodology allows a maximum exposure of 5×, the index rarely approaches that limit. To reach it, implied volatility would have to fall to exceptionally low levels, roughly comparable to a VIX in the single digits, which rarely lasts. Most of the time, exposure sits between about 1× and 2.5×, rising gradually when volatility is low and scaling back when markets become turbulent.

How CAIE manages its ladder

CAIE spreads its holdings across a laddered portfolio of autocallables with staggered start dates and strike levels. This laddering helps smooth income and reduce timing risk, since not all notes are issued, called, or matured at once.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

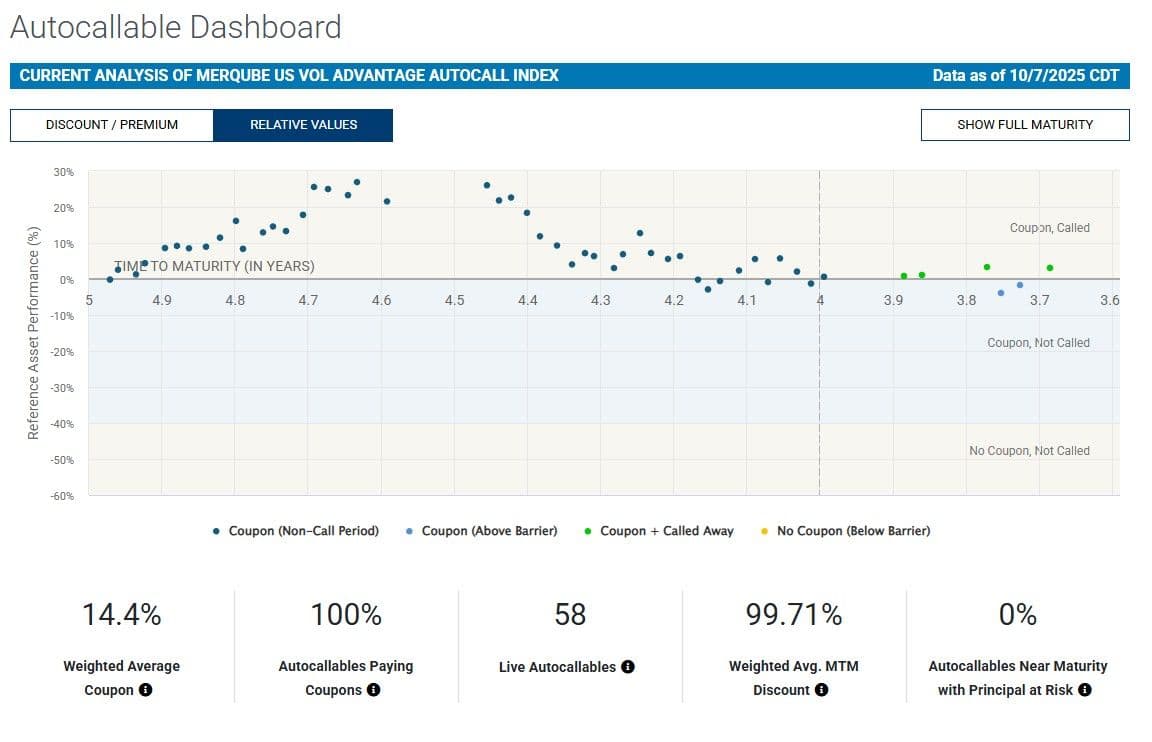

The chart below, taken from the Calamos Site, provides a snapshot of the current autocallable portfolio that powers the MerQube US Vol Advantage Autocall Index, the same framework CAIE uses inside its ETF. Each dot represents one individual note in the ladder, plotted by its time to maturity and the performance of its underlying index.

The dashboard above shows the current state of that ladder. Each dot represents one of CAIE’s active notes, plotted by time to maturity and the performance of its underlying index. Blue dots show notes still in their non-call or coupon-paying periods, green dots mark those that have been called early, and yellow dots would represent notes that have temporarily stopped paying because their index fell below a barrier. As the dots drift past the gray vertically dotted line, they become callable and as long as they're over the strike levels, they will be removed from the index with new notes being issued and appearing all the way on the left.

At the bottom, the metrics summarize the overall health of the ladder. A weighted average coupon of 14.4% shows the level of annualized income currently being earned across the portfolio. 100% of the notes are paying coupons, meaning the index is comfortably above the coupon barriers for every active position. The weighted average mark-to-market discount of 99.71% suggests that, on average, the notes are trading almost exactly at par, and 0% of the portfolio is near maturity with principal at risk, indicating no imminent exposure to losses from breached protection barriers.

In simple terms, this chart illustrates how the laddered approach helps CAIE maintain consistent cash flow while spreading risk over many observation dates and market environments. Instead of relying on a single note’s performance, the ETF’s design blends dozens of positions that are each at different points in their lifecycle, creating a smoother, more stable income stream for investors.

How Does CAIE Compare to Covered Calls?

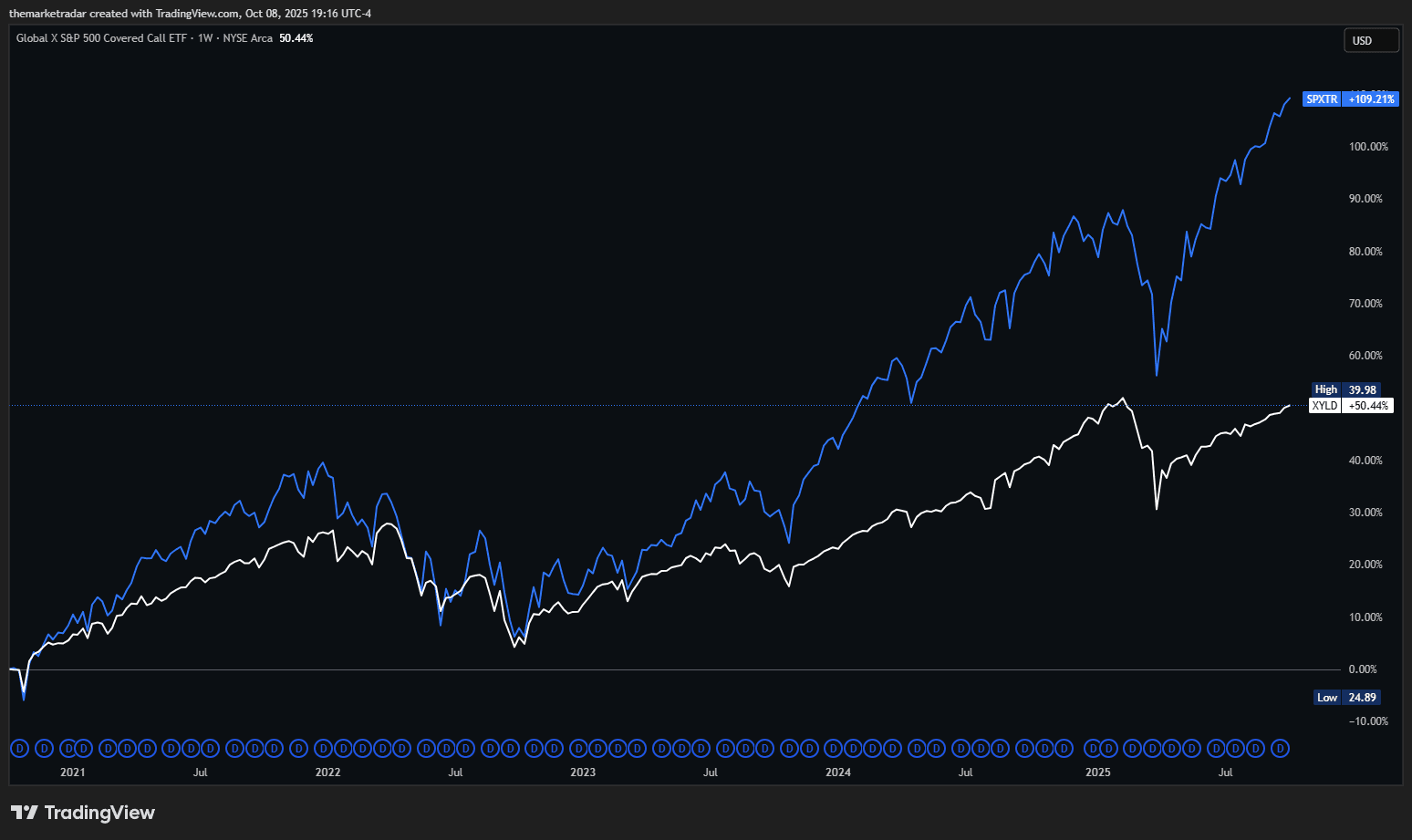

Now that you have a rounded understanding of how covered call and structured note ETFs work, let's compare them. To compare these two ETFs, we're going to have to be a little creative since CAIE only launched in 2025. CAIE tracks an underlying index called the MerQube US Large-Cap Vol Advantage Autocall Total Return Index, which has adequate history. We're going to use this as our structured note ETF proxy, XYLD as our SPX covered call ETF, and the SPX total return as our benchmark for comparison.

ONE YEAR

FIVE YEARS

TEN YEARS

Across all timeframes, the divergence is striking. The autocallable index has meaningfully outperformed the covered call strategy, particularly over longer periods and following drawdowns. The difference comes down to how each structure interacts with volatility, timing, and loss recovery.

Covered call ETFs like XYLD lock in opportunity costs almost immediately. Every month, the fund sells new call options and caps its upside at the strike price. When markets sell off, those calls expire worthless, but the fund’s equity holdings still fall in value. Then, as the market begins to recover, the ETF sells another round of calls, often at lower strike prices, effectively selling away the rebound. This constant cycle of income collection and upside limitation creates a structural headwind that compounds over time.

Autocallable structures work very differently. Their losses are conditional, not continuous. Each note’s performance is only fully assessed at maturity, typically after five years. As long as the reference index doesn’t fall more than 40% below its starting level by that final observation date, the principal is repaid in full. Short-term volatility or interim drawdowns don’t trigger realized losses; the notes simply continue paying coupons and wait for the next observation point.

This design has a powerful compounding effect. Because losses aren’t locked in during temporary market declines, autocallable portfolios can recover more effectively when markets rebound. The structure allows time for mean reversion, letting income continue to flow even through volatility. Covered call strategies, on the other hand, continuously “reset” their exposure, locking in lower strike prices and missing out on the same recovery potential.

In essence, the reason the autocallable index outperforms isn’t just higher yield; it’s structural resilience. It benefits from time and conditional protection, while covered call ETFs suffer from constant income-for-upside tradeoffs that accumulate into long-term performance drag.

How We Use CAIE

Our portfolios are inherently aggressive, so holding CAIE simply for income doesn’t make sense for us as a standalone strategy. Instead, we use it tactically, as an income enhancer during Risk-On market regimes, where conditions favor choppy or gradually rising markets rather than sharp declines. You can read more about how we define these regimes in our System.

Because our strategies are leveraged by design, we often have excess cash sitting on the sidelines when using futures instead of leveraged ETFs. To explain: in our Risk-On phases, our systems typically take leveraged long exposure in the Nasdaq-100 (NQ) and Bitcoin. Using futures gives us better control over position sizing, reduces volatility drag compared with leveraged ETFs, and offers tax advantages under U.S. futures rules. The trade-off is that futures require margin rather than full cash funding, which leaves idle cash in the portfolio that can be redeployed.

To make that cash productive, we allocate a small portion of NAV (10–15%) to CAIE during Risk-On environments. This allows us to harvest monthly dividends from the fund while maintaining our core leveraged exposures. It’s important to note that this adds incremental leverage to the portfolio overall, since CAIE itself is an equity-linked income vehicle. We’re comfortable with that, but it’s worth emphasizing that it increases both potential return and risk.

At this stage, our allocation remains modest because options on CAIE are not yet listed. As the ETF’s assets under management grow, options will likely be introduced, and that’s when the strategy becomes far more powerful. Once that happens, we plan to scale exposure to roughly 25–40% of NAV, while using long-dated protective puts to hedge downside risk. The goal is to run CAIE as a hedged yield position, collecting the fund’s monthly income while offsetting market risk through puts.

In a bull market, this setup should allow us to capture a consistent yield, benefit from gradual price appreciation in CAIE itself, and see insurance costs (put premiums) decline over time as the ETF ex-dividend drifts further from our cost basis. We’d continue harvesting the spread between dividend income and hedge cost until our system signals a shift out of Risk-On, at which point we’d close the position and return to cash. The goal isn't to capture any market appreciation on the ETF itself, but rather just the income spread.

For example, we personally started taking positions in CAIE around 26 a few months ago. Not including dividends, the ETF has appreciated on its own due to mark-to-market increases on the underlying holdings as the market has risen. In this situation, if options existed, we'd still be rolling out 26 strike puts, which are cheaper than they were a few months ago, but we're still capturing a ~14% dividend yield.

Until options are available, we’re staying nimble, running smaller allocations, monitoring signals closely, and being ready to exit quickly if conditions weaken. Drawdowns in CAIE can amplify broader portfolio losses because of our leveraged core positions, so risk control remains critical.

In short, CAIE is not just an income position for us; it’s a tactical yield engine we deploy selectively when the market backdrop supports it, integrating structured income into a broader leveraged growth framework. This space is still developing, so it's unlikely this will be the only ETF that exists, and I expect to see more issued in the future with different underlying indexes. We're using CAIE for now, but that can change when something better comes to the market.