The Squeeze Beneath the Melt-Up

Inside the Loop, Outside the Loop

In the last ledger "Two Economies, One Market" we described a cycle where enterprises are stimulating growth with their own balance sheets while the consumer runs on a separate track. Since then the System flipped into Guarded Inflation and back to full Inflation, the capex loop kept accelerating, and the april personal income release gave us a clearer read on how the consumer side is actually being funded. This Ledger walks through what changed in the dynamics, the markers worth watching for further consumer decline, and how that would feed through to the regime and the market.

The Growth Pullback Resolved

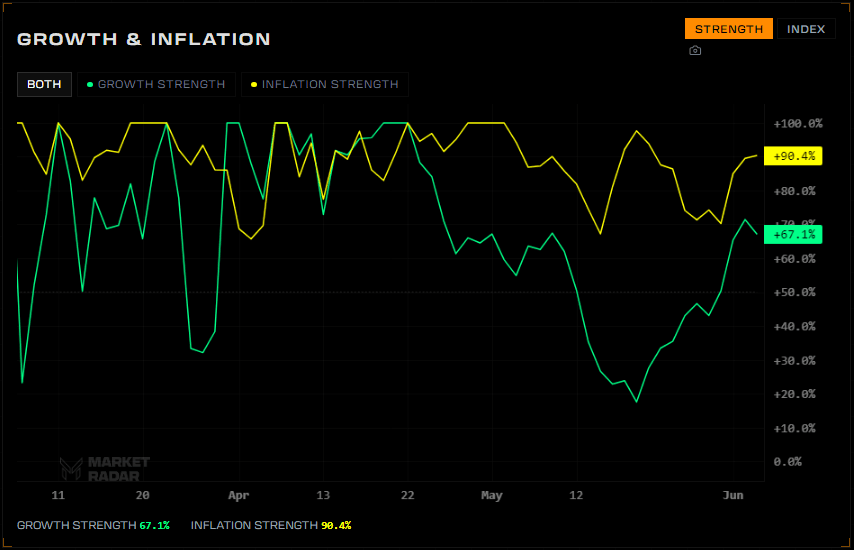

Growth strength on the System dropped to 17.5 on May 19, the lowest reading of the cycle, and the position regime flipped to Guarded Inflation. By May 20 the same reading was back to 27.6 and the regime was back to full Inflation. RQF trimmed risk for the few days we were in Guarded inflation, risks were there but never materialized, so we went back into full size.

Growth attribution over the last week shows Tech as the dominant contributor. While Consumer Discretionary continues to weigh on growth, the two economies split is showing up inside the growth signal itself.

How the Consumer Is Funding Spending

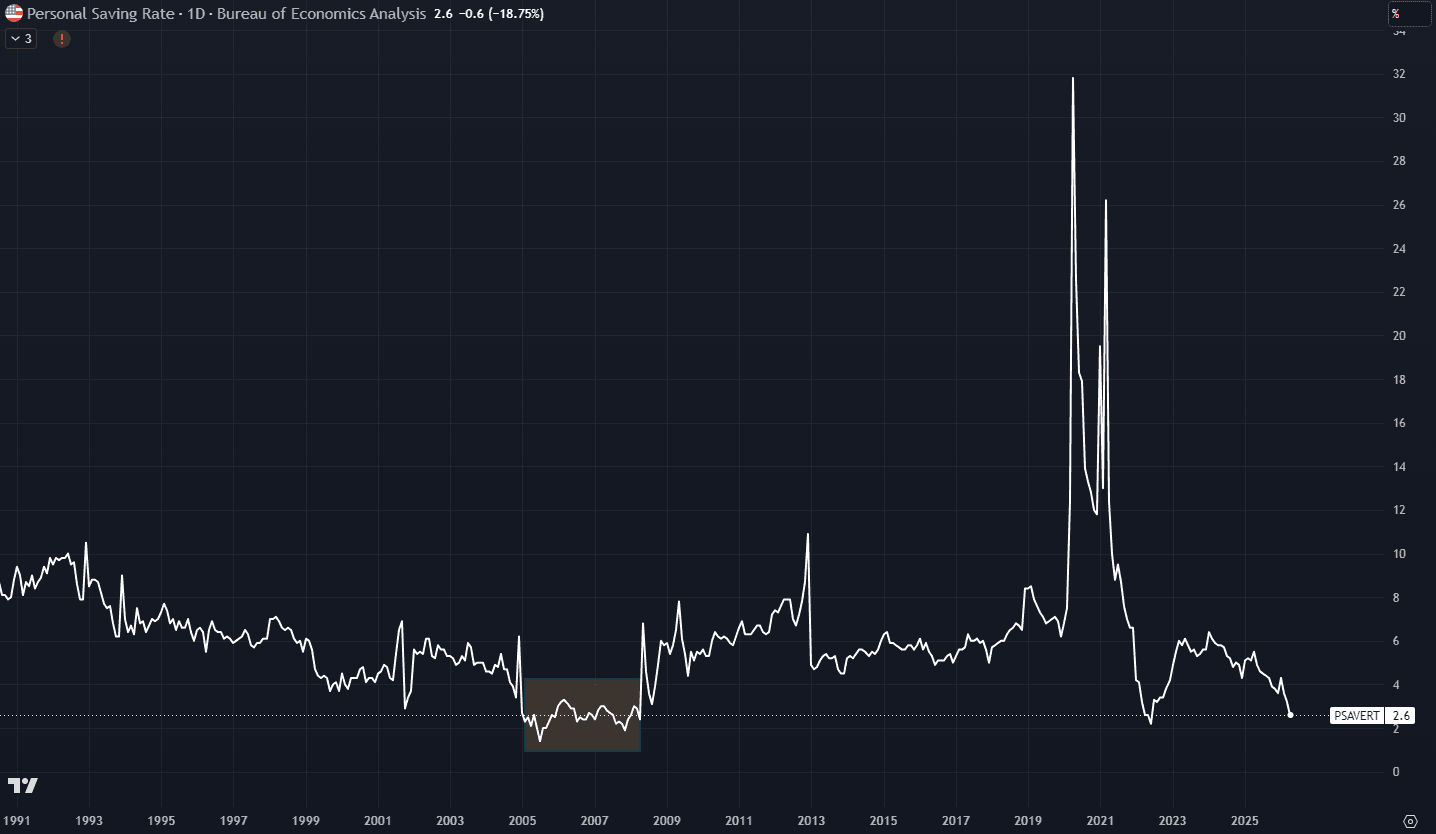

The April personal income and outlays release showed the saving rate at 2.6%, down from 3.2% in March and 3.6% in February, and from 5.5% a year ago. For context, the long-run average since 1959 is 8.4%, and the only other stretch the rate ran this low was 2005 through 2007. The level itself is worth noting, but the composition behind it is what changed.

Personal income was flat on the month and disposable personal income contracted by $19.9 billion. Nominal PCE still rose 0.5%, but real PCE rose only 0.1% and headline PCE inflation re-accelerated from 3.5% to 3.8% year-over-year. The dollar increase in spending was almost entirely price rather than volume, and with income flat, the additional spending was funded out of savings rather than out of paychecks. The consumer kept spending. The source of the spending moved from income to personal savings.

Durable goods orders came in at 0.8% against a 3.5% consensus, which fits the same picture. Durables are the discretionary big-ticket category and they soften first when households tighten. A miss of that size is an early read that the discretionary side is being trimmed even while headline spending holds.

This is the consumer side of the two-economies structure becoming legible in the data. Inside the loop, capex keeps spinning and nominal growth stays positive. Outside the loop, the household is funding flat real consumption out of savings while paying re-accelerating prices. That arrangement can run for a while. What it changes is the consumer's sensitivity to a further shock, because spending funded from a drawn-down savings pool has less room to absorb a hit than spending funded from rising income.

The Rate Channel

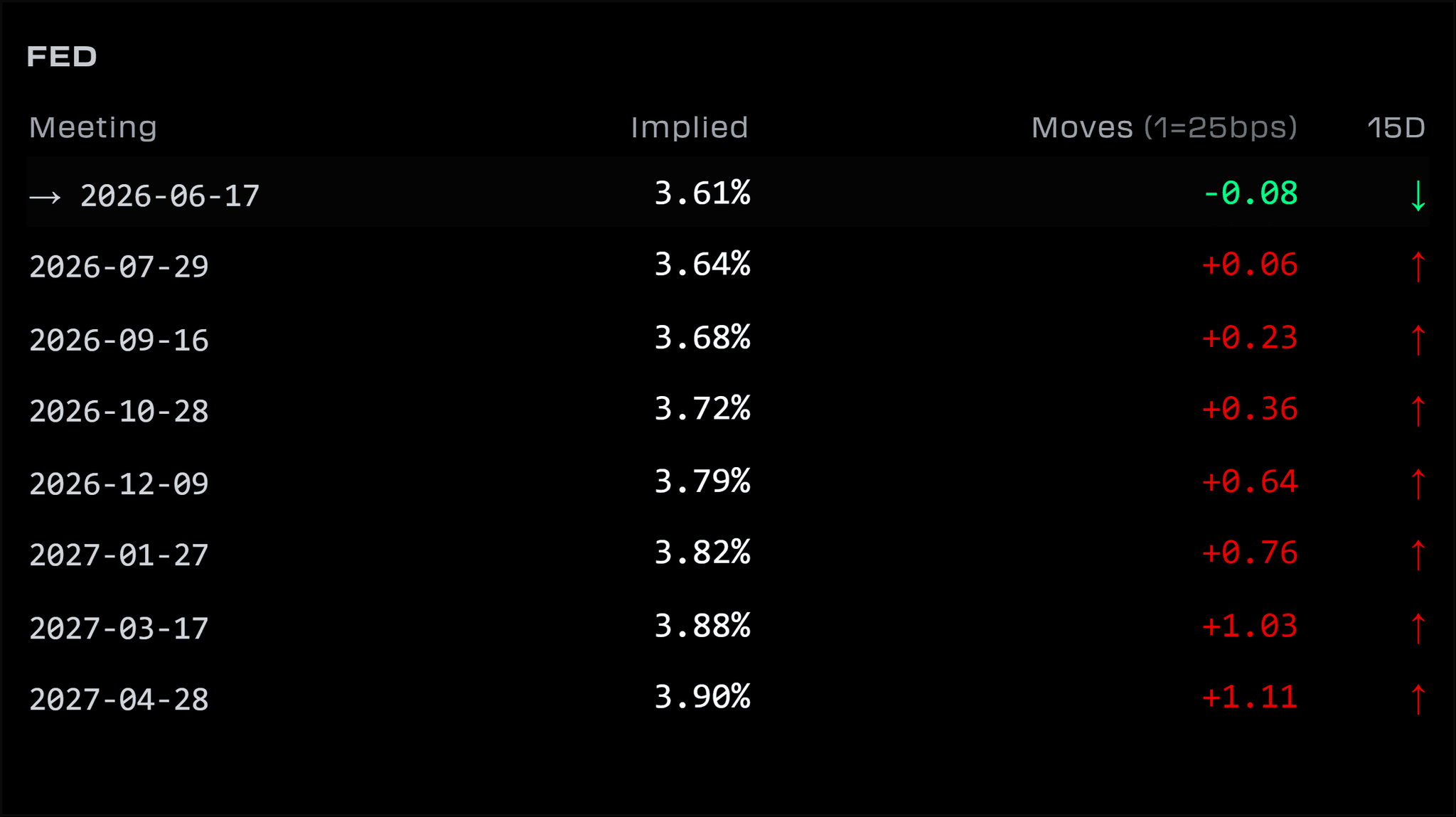

Part of why the household gets no relief on the cost side is the Fed. Fed funds futures put the implied policy rate at 3.61% through the June meeting, essentially flat with where it sits now, then climbing to 3.83% by December and 3.94% by March of next year. The curve prices roughly 80% of a 25bp hike into year-end and a full hike and then some by the first quarter of 2027. There is no net cut anywhere anymore. The April FOMC minutes line up with that pricing, with a majority of voters seeing a hike warranted if inflation persists. The hawkish tilt sits in both the official record and the futures.

For the household this means mortgages don't budge, auto financing stays expensive, and credit card APRs sit on top of an energy bill that doubled and stayed doubled. The relief valve the Fed has provided in prior consumer-stress cycles stays shut until either inflation or labor breaks. Initial claims at 225K are in line with expectations and still far below the 240K to 250K range that would signal real softening, so the labor side is holding and the Fed has cover to stay where it is.

Hormuz

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

The energy backdrop has not resolved. Oil slipped toward $87 on the latest round of deal optimism, the fifth time markets have priced a deal since March.

DBE in Ares V3 is positioned for the asymmetry. Oil bleeds out on a deal and DBE underperforms, but the equity sleeve carries the trade. Oil retests new highs on continued escalation and DBE prints into the spike. The hedge does its job without needing a directional call on the Iran outcome, and the energy cost itself is part of what keeps the household squeezed.

The Bitcoin Read

The live read on whether the loop has pulled the consumer in is Bitcoin. The trajectory from the last Ledger held. Semis up huge on the year, Bitcoin down ~25% over the same window, Risk-On readings for months, and the two assets still pointing in opposite directions.

We wrote "The Imminent Rise of Bitcoin" laying out what Astraeus needs to enter. The System has to be Risk-On and Bitcoin's DDAP trend has to flip bullish. Risk-On is satisfied. DDAP has not confirmed. Astraeus has stayed in cash through the Guarded Inflation flip, through the resolution back to Inflation, and through every bounce since the October exit at $115k.

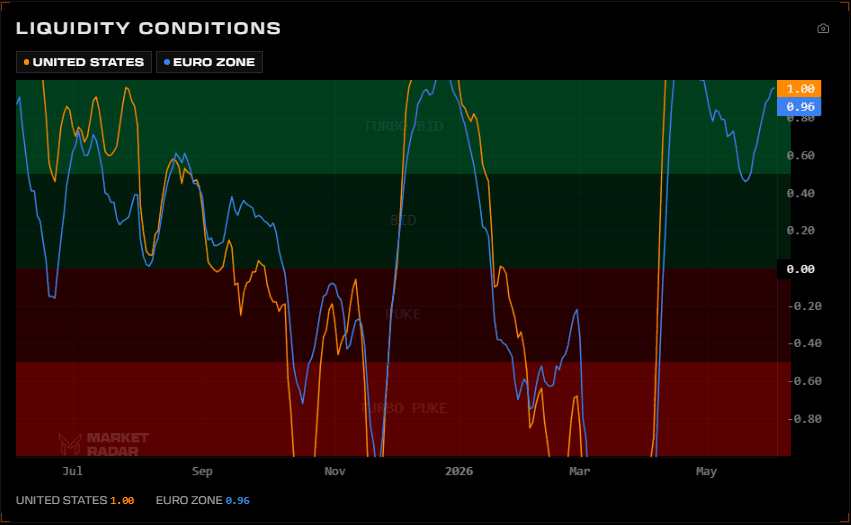

The reason it hasn't confirmed lines up with the consumer thesis. The Liquidity Conditions Index peaked on April 20 at 1.88 and has rolled to 1.06, still positive but fading. Bitcoin runs on excess liquidity overflowing past stocks and out to the far end of the risk curve, and a 2.6% saving rate means the household has little spare cash to push out there. The setup remains intact. The conditions for it to fire are a function of the same consumer dynamics, so the trigger that turns Astraeus on is also one of the cleaner signs that the stimulus loop has started reaching the consumer.

What to Watch

The consumer track and the enterprise track meet at one place, which is aggregate growth. As long as the capex loop carries the growth signal, the System stays in Inflation and consumer softness shows up only in the relative performance of consumer-facing sectors. Consumer Discretionary is already the weakest link in the growth index. The open question for the regime is whether consumer weakness deepens enough to pull the aggregate signal down with it. Three markers tell us whether that is happening.

The first is the labor market. The consumer can fund spending out of savings as long as employment and wages hold, because a job is the backstop on the income side. Initial claims at 225K say that backstop is intact. A move in claims toward the 240K to 250K range, softening payrolls, or an uptick in the unemployment rate would signal the income side starting to give, which is what turns a savings drawdown into an actual spending contraction.

The second is credit. A falling saving rate and rising revolving credit balances are the same behavior seen from two sides, so the point to watch is delinquencies. Households drawing on savings is normal late-cycle behavior. Households missing payments is where the funding mechanism strains, and that shows up in credit card and auto delinquency data ahead of spending, something that XLF may already be foreshadowing.

The third is real spending itself. Real PCE rose 0.1% in April. A move to flat or negative real PCE alongside continued durable goods misses would confirm the discretionary pullback has reached the volume side rather than just the price side.

If those markers turn together, the sequence is consumer-facing sectors underperforming first, then the aggregate growth signal weakening, then the System moving back toward Guarded Inflation and trimming risk. None of that is in the data yet. The loop is carrying growth, the labor side is holding, and the regime is in full Inflation.

Positioning

The System remains in Inflation. The Guarded Inflation flip was a one-week event that resolved cleanly, and RQF has since scaled back to full Inflation sizing. Ares V3 holds the same equity-plus-DBE structure described in "Change Is Coming." The energy sleeve is doing its job through the Hormuz whipsaw, and the tech allocation is benefiting from the continued melt-up while the model keeps the rules to trim if growth deteriorates again.

Astraeus is in cash. The regime gate is open. DDAP has not confirmed. When the trend confirms and the regime is still open, the position goes on at 2x. If the regime flips out of the eligible set first, the setup resets and we wait for the next one.

The change this month is in how the consumer is funding its spending, from income to savings, while the enterprise loop keeps carrying

aggregate growth. That arrangement holds the regime in Inflation for now.