9 MIN READ·MARCH 6, 2026

The Bull Case

MR

CO-FOUNDER · MARKET RADAR

The market is pricing in a bear case across every dimension simultaneously. NVIDIA's multiple assumes China revenue goes to zero. Software stocks (IGV) are being sold as if AI replaces every SaaS product overnight. Block's (XYZ) workforce reduction is being read as economic destruction rather than margin optimization. Iran is priced as an open-ended conflict. Gold is absorbing capital that historically flows to risk assets. And through all of this, the Magnificent 7 trade at their lowest premium to the S&P 493 in a decade.

We think the sentiment shifts have taken over reality. These sentiments are fragile, and only a few of them need to be wrong for QQQ and SPY to reprice significantly higher. Let's walk through them.

Growth Is Trading at Value Prices

Let's start with the most basic observation: growth stocks are now cheaper than defensive stocks.

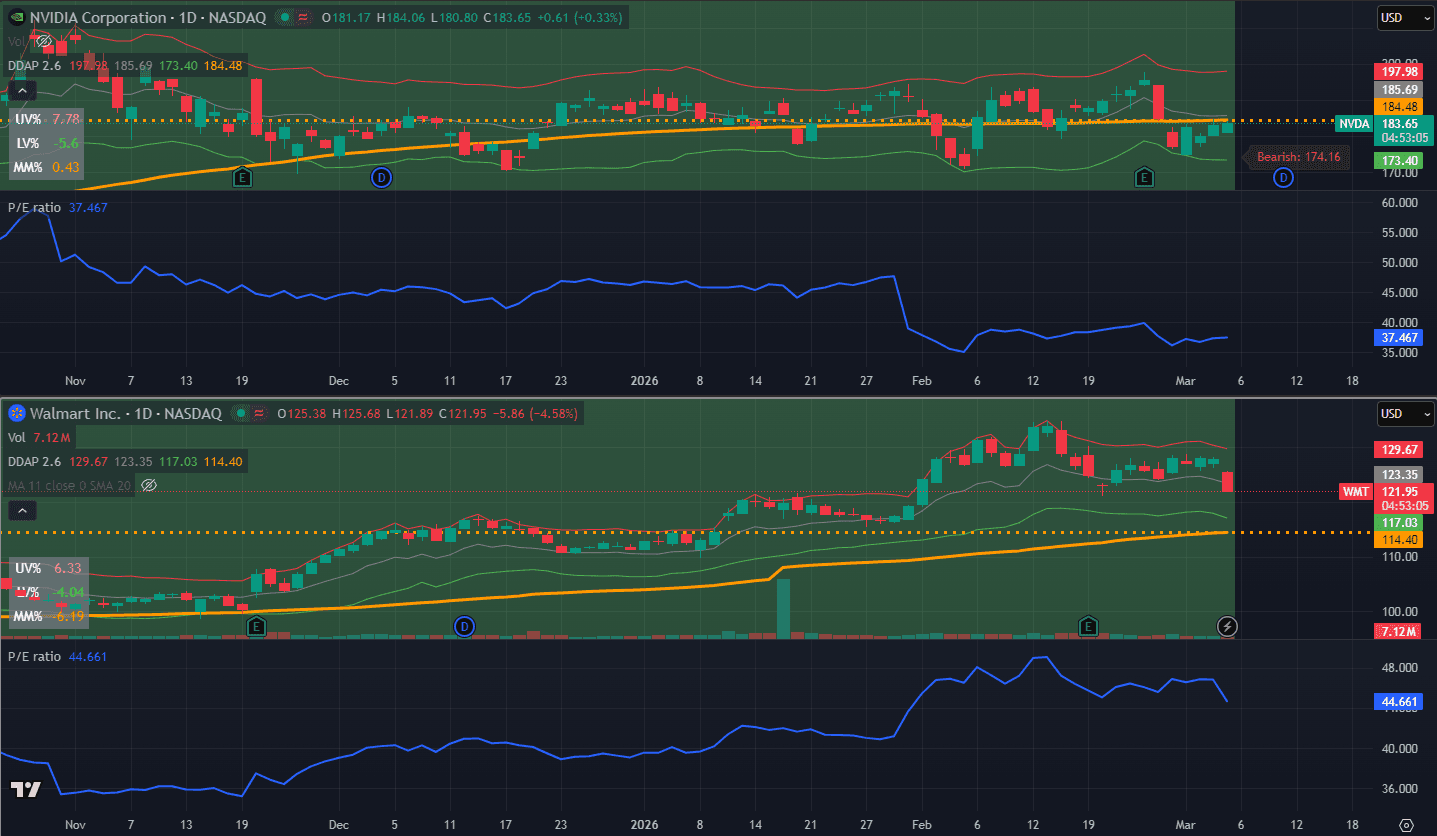

NVIDIA, the company that just printed $68.1 billion in quarterly revenue with 73% year-over-year growth, trades at 25x earnings. Netflix, growing revenue double digits with expanding margins, trades at 26x. Now compare that to the "safety" trade. Walmart commands 46x earnings. Costco trades at 54x. Consumer staples, the sector investors run to when they're scared, has become more expensive than the companies actually generating the growth.

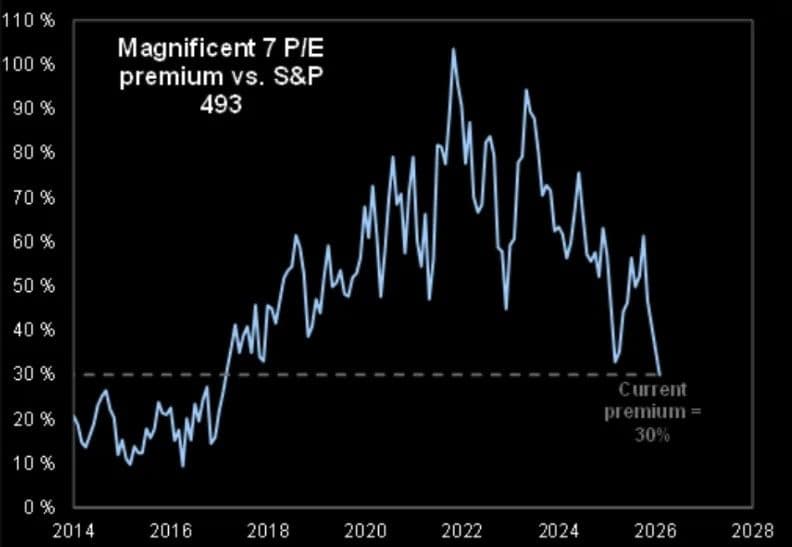

The Mag 7 premium versus the rest of the S&P 500 is sitting at a 10-year low. Meanwhile, 66% of S&P 500 companies are outperforming the index YTD. The broad market isn't weak. The Mag 7 ETF has gone nowhere for six months, and that compression is dragging the index while everything else participates. S&P Equal weight (RSP) is hovering at an all-time high. Consumer staples up 13% YTD; the Russell (IWM) is also near all-time highs. These are not things you see going into recessions. The only thing not working is mega-cap tech, and mega-cap tech is the cheapest it's been relative to everything else in a decade.

Here's Why We're Bullish The MAGS

NVIDIA

NVIDIA trades at roughly 25x forward earnings despite projecting 67% EPS growth this fiscal year.

The administration is capping H200 exports at 75,000 units per Chinese buyer, less than half of what those buyers have been requesting. AMD has already absorbed a $1.5 billion revenue hit and is now guiding on an ex-China basis entirely. The entire semiconductor industry is effectively pricing in a zero-China scenario.

But look at what NVIDIA just printed without China being a meaningful contributor. Q4 revenue came in at $68.1 billion, up 73% year-over-year and 20% quarter-over-quarter. Q1 guidance of $76-80 billion exceeded the $73 billion consensus. Free cash flow hit roughly $35 billion in a single quarter. Data center revenue has grown nearly 13x since ChatGPT's emergence, from approximately $15 billion to $194 billion annually, and hyperscalers accounted for just over half of Q4 data center revenue, meaning the customer base is diversifying rather than concentrating.

For context, during the dot-com bubble, Cisco (the market cap leader) traded at 130x earnings. NVIDIA, the current leader by market cap, trades at less than 30x with substantially faster growth. The valuation environment is completely different.

If the current multiple already prices in minimal to zero China revenue, then every incremental dollar of non-China growth, is upside the market isn't paying for. NVIDIA is the most visible case of the growth-at-a-value-price paradox. But it's not the only one.

APPLE

Apple sits on the largest installed device base on earth: over 2 billion active devices. That's the biggest potential AI distribution platform in existence, yet Apple hasn't jumped on the AI bandwagon nearly as much as the others.

Apple Intelligence is in early rollout. Unlike the hyperscalers burning tens of billions on training infrastructure each quarter, Apple's AI moat runs through on-device inference and privacy, which means near-zero incremental capex at scale. And as these AI features mature, they create a hardware upgrade catalyst that isn't in estimates yet. Users who want the full Apple Intelligence experience need newer chips to run it. That now becomes a refresh cycle driven by software capability.

NVIDIA is priced as an AI company. Apple is not. Both are critical to the AI stack. One builds the training layer. The other owns the distribution layer. Distribution tends to win over long time horizons, and the market is giving Apple no credit for it.

The broader theme here is that AI anxiety is selectively punishing some stocks while ignoring the upside for others. Nowhere is that more visible than in software.

Software: The Oversold Setup

Salesforce is down 25% year-to-date despite beating on both EPS and revenue. The selloff was driven entirely by AI disruption fears, not deteriorating fundamentals. CrowdStrike, Visa, and Mastercard have all seen sharp recent selloffs on the same thesis, that AI will replace their core business. Even companies with deep network-effect moats and recurring revenue are getting hit.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

The irony is that the CEO of the company driving the AI revolution is explicitly pushing back on this narrative. Jensen Huang has argued publicly that AI will support enterprise software, not replace it. The man building the GPUs that power the disruption doesn't agree with the disruption thesis that's crushing software stocks.

There's also a structural forced-selling dynamic making the situation worse. Roughly a quarter of the private credit market is exposed to software company buyouts that were done at peak valuations, and default rates are projected to climb multiples higher than current levels. Funds facing redemptions and potential defaults are liquidating positions indiscriminately. That's a technical overhang creating artificially depressed prices, not a fundamental verdict on software's future.

When the forced sellers exhaust and the narrative matures from "AI replaces everything" to "AI augments everything," the reversion potential in this sector is significant. And there's good reason to think the "replaces everything" read is fundamentally wrong.

AI Killing The Labour Market

Every time a resource becomes more efficient, total consumption goes up, not down. It happened with steam engines. It happened with electricity. It happened with internet bandwidth. It's happening with AI compute.

The market read DeepSeek's efficiency breakthroughs as bearish for AI infrastructure spending. The logic was simple: if you can do more with less compute, total spending on compute declines. That logic has been wrong for 200 years running.

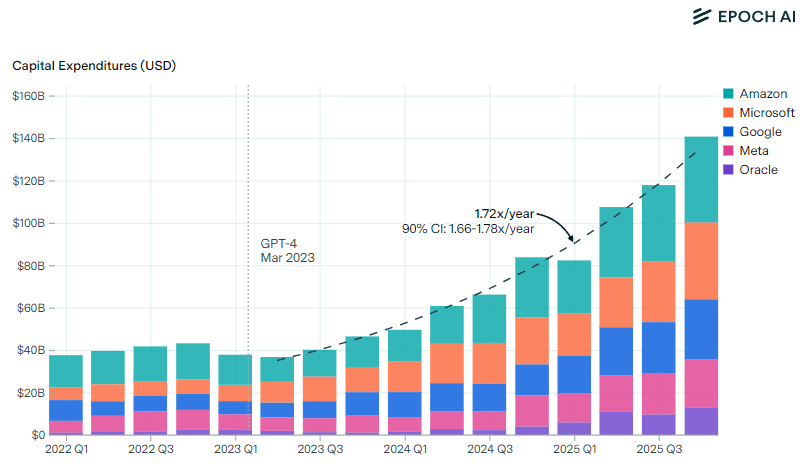

What efficiency gains actually do is unlock use cases that weren't economical before. New users, new applications, new markets. Total consumption expands even as per-unit cost declines. The hard capex data confirms this is playing out in real time. OpenAI expanded its AWS partnership by $100 billion over eight years. AMD and Meta signed an AI chips deal worth up to $100 billion over five years. Chinese buyers are requesting more than double the U.S. export cap on H200 chips, meaning demand is so strong that governments are restricting it, not because there's a surplus.

The arms race dynamic reinforces this further. Even with diminishing marginal returns per dollar of AI investment, companies cannot afford to fall behind. The competitive cost of stopping is existential. Each increment costs more, but the alternative is obsolescence.

AI capex has become a structural pillar of U.S. GDP. Remove it and the economy weakens materially. Both companies and governments have an incentive to keep the spending cycle going, which means the infrastructure buildout isn't slowing down regardless of efficiency improvements at the model layer. That spending is creating real economic activity, real jobs, and real earnings growth. Which brings us to the next mispriced fear.

Block Firing 40% Of Their Employees: Setting a Precedent?

Block announced a workforce reduction from over 10,000 employees to under 6,000. Then the headlines came in: AI is destroying jobs. The market treated it as confirmation that AI's economic impact is net-negative. It didn't help that only a few days earlier, Citrini released an article predicting this very thing to happen.

The actual numbers tell the opposite story. Q4 gross profit hit $2.87 billion, up 24% year-over-year. Cash App gross profit reached $1.83 billion, up 33%. Operating income was $485 million at a 17% margin, with adjusted operating income at $588 million and a 20% margin. Block's own guidance projects gross profit growth more than doubling from Q1 to Q4 of this year.

This is a company cutting headcount while posting record profitability and guiding for accelerating growth. That's not distress. That's optimization. The market is conflating efficiency with weakness because the layoff number makes for a better headline than the margin expansion.

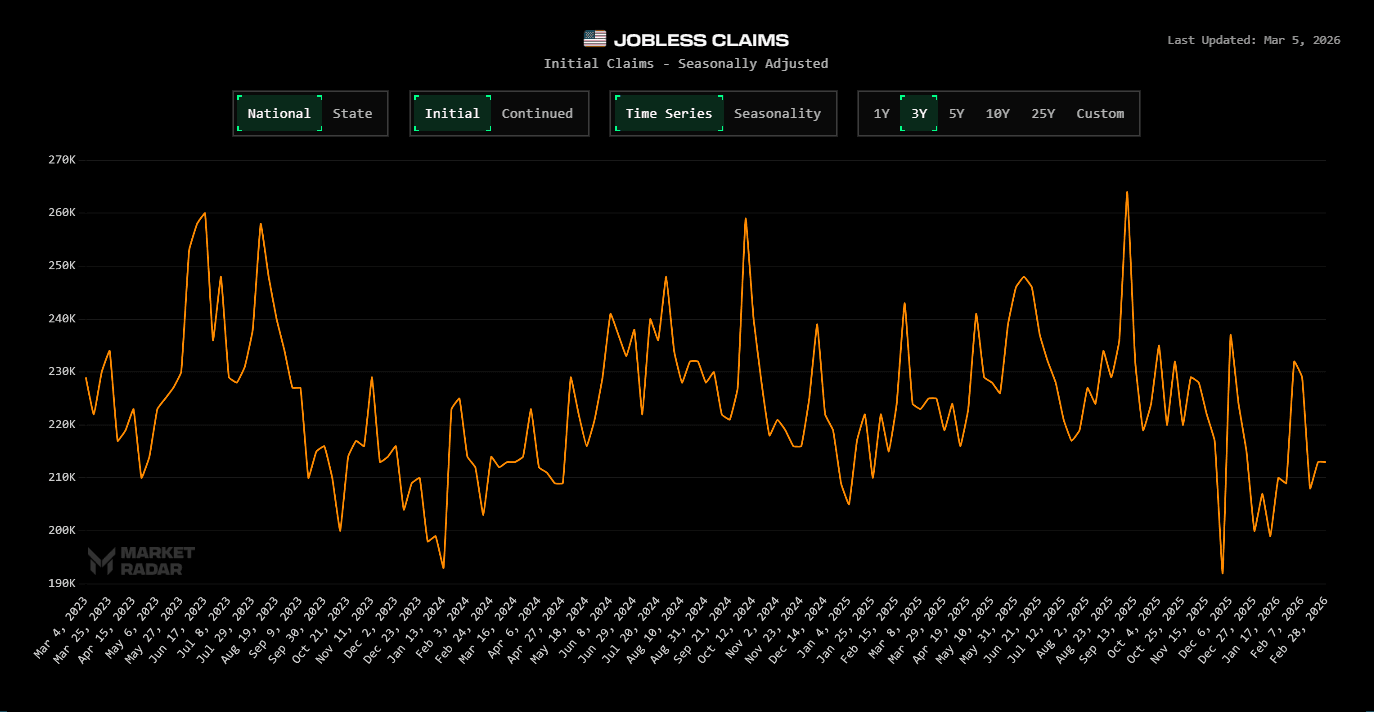

The hard labor data confirms the economy isn't cracking. Initial jobless claims printed 212,000 on February 21, sitting comfortably in a 199,000-232,000 range that has shown zero breakout tendency despite months of AI replacement fears dominating headlines. Continuing claims have flatlined around 1.9 million. If AI were actually destroying jobs at scale, these numbers would be moving. They're not. Unemployment peaked at 4.5% in November 2025 and has since declined to 4.3% in January 2026. The labor market is absorbing AI-driven restructuring without deteriorating.

For a direct counterpoint, Corning announced that the same AI infrastructure buildout is increasing their employment in North Carolina by 15-20%, sustaining a workforce of over 5,000. The AI cycle is creating and destroying jobs simultaneously. The destruction gets the headlines. The creation doesn't.

AI is in a "building the railroad" phase. Capital is being rewarded faster than labor right now. This is not a permanent structural shift. But it's being priced as permanent, which creates the mispricing. And it's not just AI anxiety weighing on sentiment. Geopolitical risk is doing the same thing.

Iran: Peak Fear, Not Peak Risk

The Iran situation looks terrifying on the surface. Operation Epic Fury, Khamenei killed, the IRGC declaring Hormuz closed, Strait traffic down 94% from normal levels, 200 tankers stranded, the Dow dropping 1,200 points intraday. We're not geopolitical analysts and won't pretend to know how this resolves.

But we can read what oil is pricing, and oil is not pricing a worst case. WTI is trading around $75 and Brent around $82. A sustained Hormuz shutdown would affect one-fifth of globally consumed oil and one-fifth of global LNG supply. If the market believed that scenario was durable, crude would be triple digits. It's not close. Saudi Arabia pre-ramped production by roughly 500,000 barrels per day ahead of the strikes, OPEC+ agreed to boost output by 206,000 bpd starting April, and OPEC spare capacity sits at 3.5 million bpd, mostly concentrated in Saudi Arabia and the UAE. Iran's entire naval fleet in the Gulf of Oman was destroyed within 48 hours. When maritime insurers pulled war risk coverage and supertanker rates hit a record $424,000 per day, Trump directed the DFC to provide government-backed insurance for all Gulf maritime trade and offered Navy escorts for tankers. Oil pulled back on the announcement.

Iran uncertainty has been weighing on this market for weeks, well before the first strike landed. The threat of conflict, the failed negotiations, the ambiguity of what comes next, that overhang suppressed risk appetite across the board. Now that the conflict is here and the trajectory is visible, certainty is replacing ambiguity. Trump has stated an expectation of four to five weeks. Iran's ability to project force is being dismantled in real time. The odds of an upside surprise, a faster resolution, a ceasefire, a collapse of resistance, are materially higher than the odds of sustained escalation with a navy that no longer exists. Eventually Iran risk comes off the table entirely, and when it does, that weight lifts from equities.

So we have multiple individual reasons to think the market is ready to bounce like a beach ball held under water. But individual stories need a macro backdrop to matter. Our system collates and quantifies many variables much better than we can ever do manually. Here's what our proprietary model says about the foundation underneath all of them.

What Our Models Are Signaling for What Comes Next

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access