13 MIN READ·JANUARY 18, 2026

Tariff Rulings: Maybe No Outcome Is Best

MR

CO-FOUNDER · MARKET RADAR

Tariff Purgatory

The Supreme Court keeps dodging the biggest trade policy decision in a generation. Markets keep waiting. And here's the uncomfortable truth: the longer this drags on, the better it might be for risk assets.

On Wednesday, the justices issued three opinions. None of them addressed the $180 billion question hanging over every portfolio in America. Equities sold off into the close. Bonds caught a bid. And the legal foundation for Trump's entire tariff regime remains suspended in constitutional limbo. This is not a new pattern. The Court passed on the decision last Friday, January 10th, and the week before that. Every time markets brace for clarity, they get more limbo. At this point, observers expect a ruling sometime between now and the Court's June term, though many anticipate it sooner, given the magnitude of what's at stake.

The case, formally known as Learning Resources, Inc. v. Trump, has become a flashpoint for how the executive branch can wield emergency powers and what happens when those powers collide with Congressional authority over taxation. If IEEPA tariffs are struck down, importers could be owed hundreds of billions in refunds. If they're upheld, the president gains sweeping new authority to tax global trade without Congress.

We're going to walk through exactly what's being contested, how each outcome bleeds into the economy, and why the current state of paralysis may actually be the most constructive setup for risk assets in the near term.

What's Actually On Trial

The core issue is straightforward: Trump bypassed Congress to impose these tariffs using the International Emergency Economic Powers Act (IEEPA). This law, enacted in 1977, was designed to allow the president to respond to foreign threats through sanctions, asset freezes, and trade restrictions during declared national emergencies. The statute grants authority to "regulate" or "prohibit" imports. What it does not do, at least not explicitly, is authorize the imposition of tariffs, which are a form of taxation reserved for Congress under the Constitution.

No president had ever used IEEPA to levy tariffs until Trump invoked it on April 2nd, 2025, the day he called "Liberation Day." He declared the trade deficit a national emergency and imposed sweeping "reciprocal tariffs" on nearly every country that trades with the United States. Rates ranged from 10% to over 50%, depending on the bilateral trade balance with each partner. Additional IEEPA tariffs were layered on top of Canada, Mexico, and China under the justification of curbing fentanyl trafficking and illegal immigration.

The administration continues to lean on IEEPA even as the case pends. Just today, Trump announced 10% tariffs on eight NATO allies, effective February 1st, explicitly tied to forcing a deal on Greenland. Denmark, Norway, Sweden, France, Germany, the UK, the Netherlands, and Finland would see rates escalate to 25% by June 1 if no agreement is reached for "the complete and total purchase of Greenland." The announcement came hours after European military personnel arrived in Nuuk for joint Arctic exercises, which Trump characterized as a "very dangerous situation for the safety, security, and survival of our planet."

Here's the critical connection: if the Supreme Court strikes down IEEPA, these Greenland tariffs are dead on arrival. The ruling isn't just about unwinding existing policy. It's about whether the president retains tariffs as a geopolitical weapon. NBC News noted in its coverage that "it was not immediately clear under what authority the new tariffs would be applied," given that existing tariffs on the UK and EU were imposed using IEEPA. In other words, the administration is betting on a favorable ruling or at minimum continued legal limbo while it escalates pressure on European allies.

Both the Court of International Trade and the Federal Circuit Court of Appeals ruled against the administration. In August 2025, the appeals court determined in a 7-4 ruling that IEEPA's grant of authority to "regulate" imports does not equate to the power to impose tariffs. The Supreme Court agreed to hear the case in September and held oral arguments on November 5th. During those arguments, justices from both the conservative and liberal wings expressed skepticism about the administration's position that Congress could or would delegate such unbounded taxation power to the executive. As one legal observer from the Peterson Institute noted, the reciprocal tariffs represent "an end-run around Congress's chosen framework."

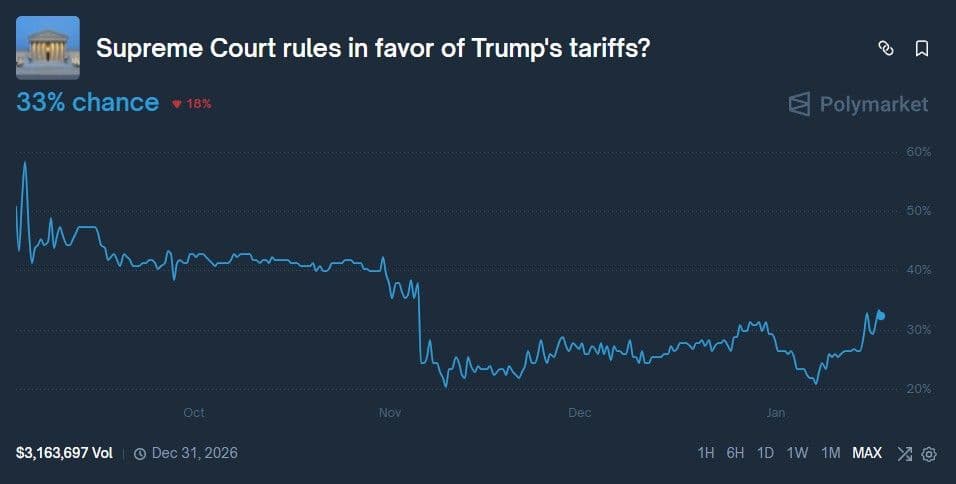

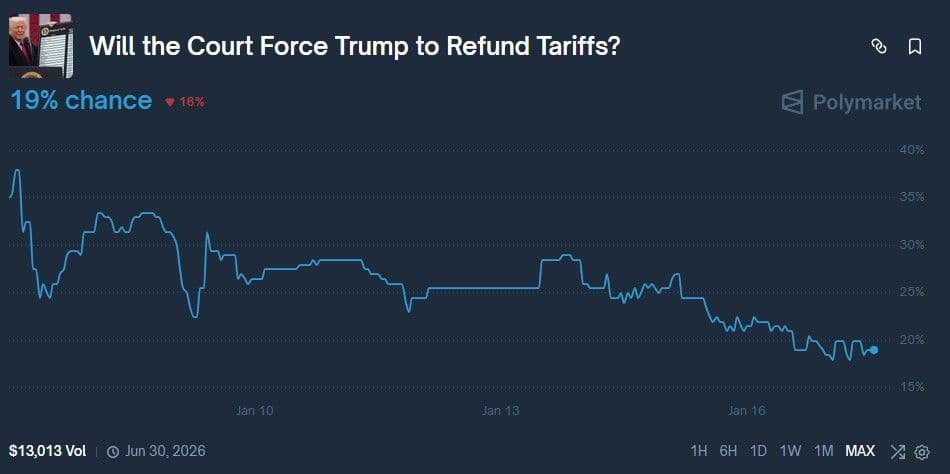

Online betting markets now assign roughly 30% odds that the Court will uphold the tariffs and roughly 20% odds that refunds will be administered. The consensus expectation is that IEEPA gets struck down in some form, but refunds don't happen. The question is what happens next, both to the $180 billion already at stake and to the administration's ability to impose new tariffs like those threatened against Denmark and its allies.

The $180 Billion Breakdown

Not all tariffs are at risk. Only those imposed under IEEPA are subject to this ruling. According to J.P. Morgan, IEEPA measures account for approximately 61% of the year-to-date increase in U.S. tariffs, translating to about $180 billion in annualized revenue as of late 2025. The Tax Foundation estimates IEEPA tariffs will raise an additional $1.2 trillion over the next decade on a conventional basis, though dynamic scoring that incorporates economic drag reduces that to about $880 billion.

Here's how the at-risk tariffs break down:

The reciprocal tariffs from Liberation Day, which imposed rates between 10% and 50% on most trading partners, account for roughly $80 to $100 billion in annual revenue. The China fentanyl tariffs (10%) contribute another $40 to $50 billion. The Canada tariffs (35%) and Mexico tariffs (25%) together represent roughly $16 to $24 billion. The elevated tariffs on Brazil (40%) add another $2 to $3 billion. India faces a combined 50% rate due to both reciprocal tariffs and penalties for Russian oil imports, contributing $3 to $5 billion.

By contrast, tariffs that are NOT at risk, because they were imposed under different legal authorities (primarily Section 232), include steel (50%), aluminum (50%), autos and auto parts (15% to 25%), legacy China tariffs from Trump's first term (7.5% to 25%), and lumber. These tariffs went through proper procedural channels, with Commerce Department investigations and formal findings of national security threats. Together, they represent roughly $100 billion in annual revenue and would remain in effect regardless of how the Supreme Court rules on IEEPA.

Treasury data shows approximately $195 billion collected in fiscal 2025 and another $62 billion in fiscal 2026 to date. If IEEPA tariffs are struck down and the government is ordered to issue refunds, the Department of Justice has confirmed in court filings that reimbursements would apply to all levies imposed under the statute, including those on Brazil and India that were not part of the original lawsuits. "In other words, although we reserve our right to challenge specific complaints, generally a properly raised IEEPA tariff challenge would be subject to the stipulation," federal attorneys wrote.

Over 301,000 importers of record have filed more than 34 million entries of goods subject to IEEPA tariffs, resulting in an estimated $129 billion in additional duty deposits. One justice described the refund situation as a "mess" during oral arguments.

Scenario One: IEEPA tariffs are deemed illegal, and all tariff revenue must be refunded.

This is the most disruptive outcome. The government would be on the hook for potentially over $100 billion in refunds to importers. According to the Tax Policy Center, if IEEPA tariffs are overturned without replacement, the average tariff rate would decrease by about 8 percentage points, from roughly 17% to 5%. That 5% rate is still double pre-2024 levels, but represents a meaningful reduction in import costs.

For equities, the initial reaction is likely positive. Wells Fargo estimates a ruling against tariffs would boost S&P 500 earnings before interest and taxes by 2.4% in 2026. Consumer-facing companies, importers, apparel makers, toymakers, and financials would benefit most. The S&P 500 Consumer Staples Index jumped as much as 2.3% on Thursday alone as speculation mounted about an imminent ruling, the biggest gain since April's Liberation Day reversal rally.

But here's where the backup plan kicks in. The administration has been explicit: Treasury Secretary Bessent has stated the White House has "at least three other options through the 1962 Trade Act that will keep most of the tariffs in place." The moment IEEPA falls, the clock starts on alternative legal pathways.

The most immediate tool is Section 122 of the Trade Act of 1974. It allows the president to impose tariffs up to 15% for 150 days to address balance-of-payments deficits. No investigation required, no public comment period. According to the Tax Policy Center, Section 122 would raise $112 billion more in 2026 than if IEEPA were overturned without replacement. The administration could invoke it within days of an adverse ruling.

The problem is duration. Section 122 tariffs expire after 150 days unless Congress extends them. That creates a window of uncertainty where importers rush to front-run expiration, supply chains get whipsawed, and markets have to price a constantly shifting tariff regime. Brookings research notes that while Section 122 provides immediate coverage, it represents a "much weaker legal foundation" that could invite additional court challenges.

Beyond Section 122, the administration would pivot to Section 232 of the Trade Expansion Act of 1962 for medium-term coverage. Section 232 allows tariffs on imports that threaten national security, with no cap on rates or duration. The catch is process: Commerce Department investigations must be completed within 270 days, followed by a 90-day presidential decision window. That's nearly a year before new 232 tariffs could take effect. However, the administration has already been laying groundwork. According to Skadden, at least seven categories of goods are currently under Section 232 investigation, including semiconductors, pharmaceuticals, and critical minerals. If IEEPA falls, expect those investigations to accelerate.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Section 301 of the Trade Act of 1974 provides another avenue. It allows the U.S. Trade Representative to investigate and remedy unfair trade practices by specific countries. Unlike IEEPA, Section 301 has a strong legal foundation, with courts having upheld previous actions against China for intellectual property theft and forced technology transfer. The limitation is scope: Section 301 can only target specific unfair practices by specific countries. It cannot replicate the universal "reciprocal" tariff framework that IEEPA enabled. USTR has already initiated a Section 301 investigation into Brazil, looking at trade and IP policies, deforestation practices, and ethanol market access.

For bonds, a full refund scenario initially pressures yields higher as fiscal deficit concerns resurface. JPMorgan strategists note that tariff removal would "rekindle fiscal concerns, presenting a risk of higher long-term yields and steeper curves." However, Morgan Stanley expects any selloff to be short-lived: "The second order and more lasting reaction is investors 'buy the fact' and send yields lower."

The economic impact: TPC estimates tariff removal would save families an average of $1,200 in 2026 and reduce taxes on households by $1.4 trillion over ten years. But that relief would be temporary as backup tariffs phase in.

Scenario Two: IEEPA tariffs are deemed illegal, but no refunds are required.

This is possible under a legal doctrine called "prospective overruling" or "sunbursting," established in the 1932 case Great Northern Railway Co. v. Sunburst Oil. Under this approach, the Court would invalidate the use of IEEPA for tariffs going forward but not require the government to reimburse what was already collected.

Treasury Secretary Bessent has publicly speculated about a "mishmash" ruling of this nature. Morgan Stanley analysts agree there is "significant room for nuance" in how the Court approaches this case. The justices could narrow the scope of existing tariffs without mandating full removal, or limit the future application of IEEPA while allowing current tariffs to stand temporarily.

The fiscal implications here are much less severe. The government keeps the $129 billion already collected. Deficit concerns stay muted. Bond markets breathe easier. But the effective tariff rate still declines going forward, and the administration still needs to pivot to alternative authorities to maintain its tariff regime.

The backup plan execution is identical to Scenario One, but with less urgency. Without refund obligations, Treasury has more fiscal runway to manage the transition. Section 122 could be deployed immediately as a bridge, with Section 232 and 301 investigations running in parallel. Nomura's David Seif has stated that "certainly by the end of 2026, we would have a tariff regime that looks almost exactly the same as what is there." The path just becomes longer and more procedurally complex.

Scenario Three: IEEPA tariffs are legal and remain in place.

This is what the administration is hoping for, but market expectations suggest it's the least likely outcome at roughly 30% probability. If the Court upholds Trump's use of IEEPA, it would establish a precedent granting the executive branch sweeping tariff authority under emergency powers, a constitutional expansion of presidential power that several justices appeared uncomfortable with during oral arguments.

The immediate economic implications are straightforward. Tariff revenue continues flowing to the Treasury at the current $195 billion annual pace. Import costs remain elevated. The effective tariff rate stays near 17%, compared to 2.6% before Liberation Day. Inflation pressures persist, particularly in consumer goods categories dependent on imports.

The labor market continues to suffer. Mark Zandi at Moody's Analytics has noted that since Liberation Day, there has effectively been no job growth in the United States. Manufacturing has hemorrhaged 70,000 jobs since April. The 2025 jobs report showed only 584,000 jobs added for the full year, the weakest outside of recession since the early 2000s. "The global trade war's fingerprints are all over the ailing job market," Zandi stated.

For bonds, this scenario is relatively supportive. Fiscal concerns ease as tariff revenue keeps flowing. The 30-year yield, currently around 4.5%, stays below the cycle highs reached in mid-2025. But growth headwinds persist, meaning duration ultimately benefits if the economic deterioration continues.

The administration retains maximum flexibility in this scenario. No need for backup plans. No procedural scramble. The tariff threat remains credible for ongoing trade negotiations, including the USMCA renegotiation scheduled for this year.

Scenario Four: A partial or nuanced ruling.

This may be the most likely outcome given the complexity of the case and the diverse concerns expressed by justices during oral arguments. The Court could rule that IEEPA authorizes some tariffs but not others. For example, it might uphold the fentanyl-related tariffs on Canada, Mexico, and China (which have a clearer national emergency justification) while striking down the reciprocal tariffs (which are harder to justify as emergency measures since trade deficits are neither unusual nor clearly emergencies).

Alternatively, the Court could limit future IEEPA tariff authority without fully unwinding existing measures. It could require the administration to provide clearer national emergency justifications for specific tariff actions. It could cap the rates or duration of IEEPA tariffs. The possibilities are numerous.

The backup plan response depends entirely on which tariffs survive. If reciprocal tariffs fall but fentanyl tariffs remain, the administration would have about $80 to $100 billion in annual revenue at risk, requiring Section 122 as an immediate bridge and accelerated Section 232/301 investigations to rebuild the framework. If all IEEPA tariffs are narrowed to specific products rather than blanket country-level duties, the administration might pivot to Section 338 of the Tariff Act of 1930, a Depression-era provision that allows tariffs up to 50% on imports from countries engaging in discriminatory practices. Section 338 has never been used before, and any attempt would almost certainly face immediate legal challenges.

Markets would need to reprice the path forward in real-time, likely producing elevated volatility as clarity emerges gradually rather than all at once. The administrative burden on Customs and Border Protection would be substantial as different tariff authorities get layered, creating compliance complexity for importers.

Why Limbo Might Be the Best Case

Here's where we come to the uncomfortable conclusion. Given the range of outcomes and the certainty of messy transitions regardless of which way the ruling goes, the current state of limbo may actually be the most constructive setup for risk assets in the near term.

If the Court strikes down IEEPA, we trade one uncertainty for another. The administration will scramble to invoke Section 122 immediately, creating a 150-day window of temporary coverage. Section 232 and 301 investigations will accelerate. Importers will rush to bring goods in before new tariffs take effect, creating supply chain distortions. The fiscal picture becomes murkier as tariff revenue becomes less predictable. Markets will need to reprice constantly.

If the Court upholds IEEPA, the tariff headwinds persist. Growth continues to struggle under elevated import costs. Labor markets remain under pressure. Earnings face margin compression. The case for a sustained equity rally becomes harder to make without the relief valve of lower tariffs.

However, as long as the decision remains in legal limbo, both sides can continue to operate under their preferred assumptions. Equities can trade on the hope of eventual relief. Bonds can trade on the assumption that tariff revenue continues flowing for now, keeping deficit concerns at bay. Neither outcome has crystallized, so neither downside is fully reflected in the price.

The market reaction to this week's postponement confirmed that dynamic. Stocks sold off because they want the ruling and expect it to be favorable. Bonds caught a bid because a delay means more time for tariff revenue to accumulate and less urgency around refunds.

In short, resolution forces positioning. Limbo allows ambiguity. And in a market already navigating slowing growth, sticky inflation, and elevated policy uncertainty, ambiguity may be the lesser evil.

The Regime Has Shifted

While the tariff case has dominated headlines, our System has been telling a different story. As of January 6th, the...

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access