Everything You Need to Know About Today's FOMC

Market Positioning

Today’s FOMC meeting delivered further clarity on what the Fed is watching before it pushes further on easing, and the market’s reaction is telling us a bigger story than the headlines. We'll dig into what the market was expecting coming into FOMC, what the SEP tells us, key highlights from Powell, and the implications we see going forward.

In the weeks leading up to this meeting, investors were already betting on signs of a labor slowdown. TLT ripped 5% following the softer-than-expected NFP, and the -911k labor revision added conviction to that view. The terminal rate has steadily drifted down toward 2.8%, yet equities have kept grinding higher. That strength, paired with a sharp rally in Gold, suggests a market that sees these cuts less as an emergency response and more as a potential policy misstep, one that could ultimately fuel both growth and inflation.

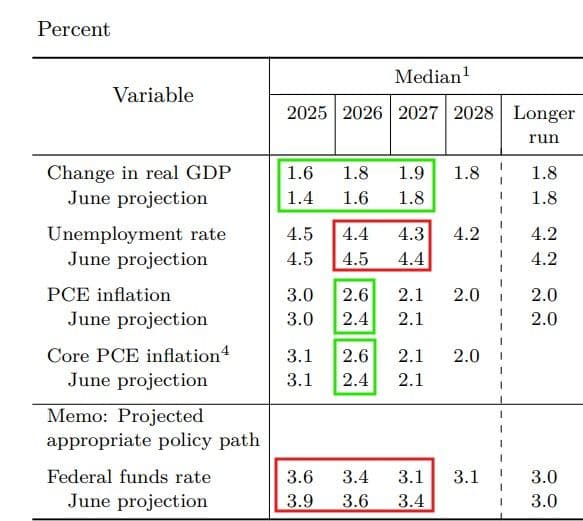

Summary of Economic Projections

This FOMC meeting was also a meeting where economic projections were given, known as a Summary of Economic Projections (SEP) meeting. These projections give insight into how the Fed members are seeing growth and inflation projections over the next few years. This is an important tool the Fed has in issuing forward guidance that goes beyond simple FOMC statements and press release Q&As.

What we saw today was quite incredible. As we mentioned earlier, the market was somewhat dovish into today’s event. Fears of a slowdown in the labor market have been quite rampant, and they have everyone on their toes, including the Fed. This is where things get interesting, though.

Looking at the Fed’s table of economic projections within their SEP, you’ll see the following:

- Median real GDP was revised higher every year since the June estimates.

- Both median core and headline PCE were revised higher for 2026.

- Median unemployment was revised lower for 2026 and 2027.

- Fed funds rate path has been revised lower every year since the June estimates.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

If you take another look at the table, the Fed is indicating its policy will continue to drift lower over the next three years, at a faster rate than what was implied in June. The key here is to understand that the market front-ran a lot of this. As we mentioned earlier, bonds have been rallying, and the terminal floor has been falling over the last few months. The market was more in line with the expectations; they were not surprised by them.

What is clear is that the Fed still isn’t buying the labor market breakdown. You’re seeing minimal shifts to unemployment expectations; instead, you’re seeing signs of growth and inflation expectations reaccelerating. The SEP confirms the forward guidance the market was pricing in, and it seems the Fed is going to continue reducing policy rates despite a resilience in growth and inflation.

Press Conference

The Chairman of the FOMC is responsible for delivering press statements and answering questions after each meeting. This part of the day provides a second layer of forward guidance, which is why markets pay such close attention to it. Earlier in the day, the SEP leaned dovish. It showed the Fed preparing to lower policy rates based on only a small increase in unemployment expectations, while also raising both growth and inflation projections. That report was released 30 minutes before the Chairman spoke, shaping market sentiment heading into the press conference.

During his remarks, we got the full picture of the Fed’s outlook. He described today’s rate cut as a “risk management cut,” emphasized that unemployment remains “low,” and explained that the nearly 911,000 downward revision in job numbers (QECW) was close to what the Fed had already expected. His tone was more hawkish than the SEP suggested, signaling that the Fed was not as surprised by the weak jobs data as many in the market had assumed. He also made it clear that the Fed does not need to move quickly on rates, reinforcing the idea that the central bank will take a cautious approach. Earlier this month, some analysts argued that if the Fed had known about the near one million job revision sooner, they would have cut much more aggressively. Powell’s statement pushed back on that view by showing that the Fed still judged a 25bps cut to be sufficient. Even after factoring in the job revisions, the Fed continues to see unemployment as “low,” and framed this decision as a cautious adjustment rather than a necessary move.

So what does today’s FOMC actually mean for markets?

In many ways, the outcome was already priced in, which explains why equities finished the day mostly flat. The probability of a near-term melt-up has narrowed, since that would require a clear policy mistake, specifically, rates easing too quickly. One possible path to that scenario is if the recent labor weakness proves to be another head fake, much like August 2024. In that case, the Fed would be cutting into an economy that is actually re-accelerating. The result would be higher long-end yields, stronger risk assets, and renewed upward pressure on inflation, with recession fears fading into the background. Given we're in a strong Risk-On regime at the moment, we see this as a likely outcome.

Right now, our neutral rate estimates suggest the Fed is about 25 basis points below neutral. In simpler terms, forward guidance of policy is already one cut into accommodative territory as the rate-cutting cycle begins. Normally, you would expect this spread to turn positive during a genuine economic slowdown or recession, because that shift signals the Fed intends to loosen policy to stimulate financial conditions as growth weakens.

The issue comes if the economy proves resilient and begins to reaccelerate. In that case, the Fed risks becoming accommodative too quickly, cutting rates more than necessary while the market responds with stronger momentum. This creates a lag in the Fed’s ability to regain control over forward guidance, shifting investor concerns from recession risks to doubts about the Fed’s capacity or willingness to control inflation.