Disinflation Is The Bull Case

The enterprise loop continues to provide stimulus to everything within the loop, while the consumer runs on a separate track with no relief on the cost side. The consumer has been getting chewed up by high energy costs and a frozen rate curve. The recent peace deal opens the energy jaw, and the rate jaw with it. The policy path was priced up on the war over fears of energy inflation getting further entrenched into CPI, and unwinding it eases conditions on its own, without any cuts required.

But the rally off the lows is borrowed, not earned. The last two months have climbed a wall of worry built on one thing: a deal landing, and the deal is here now. The last 90 days won't be the next 90 days. This only converts to a sustainable bull if it carries us into expansion. A simple return to the inflation regime is the wrong outcome, and here’s why.

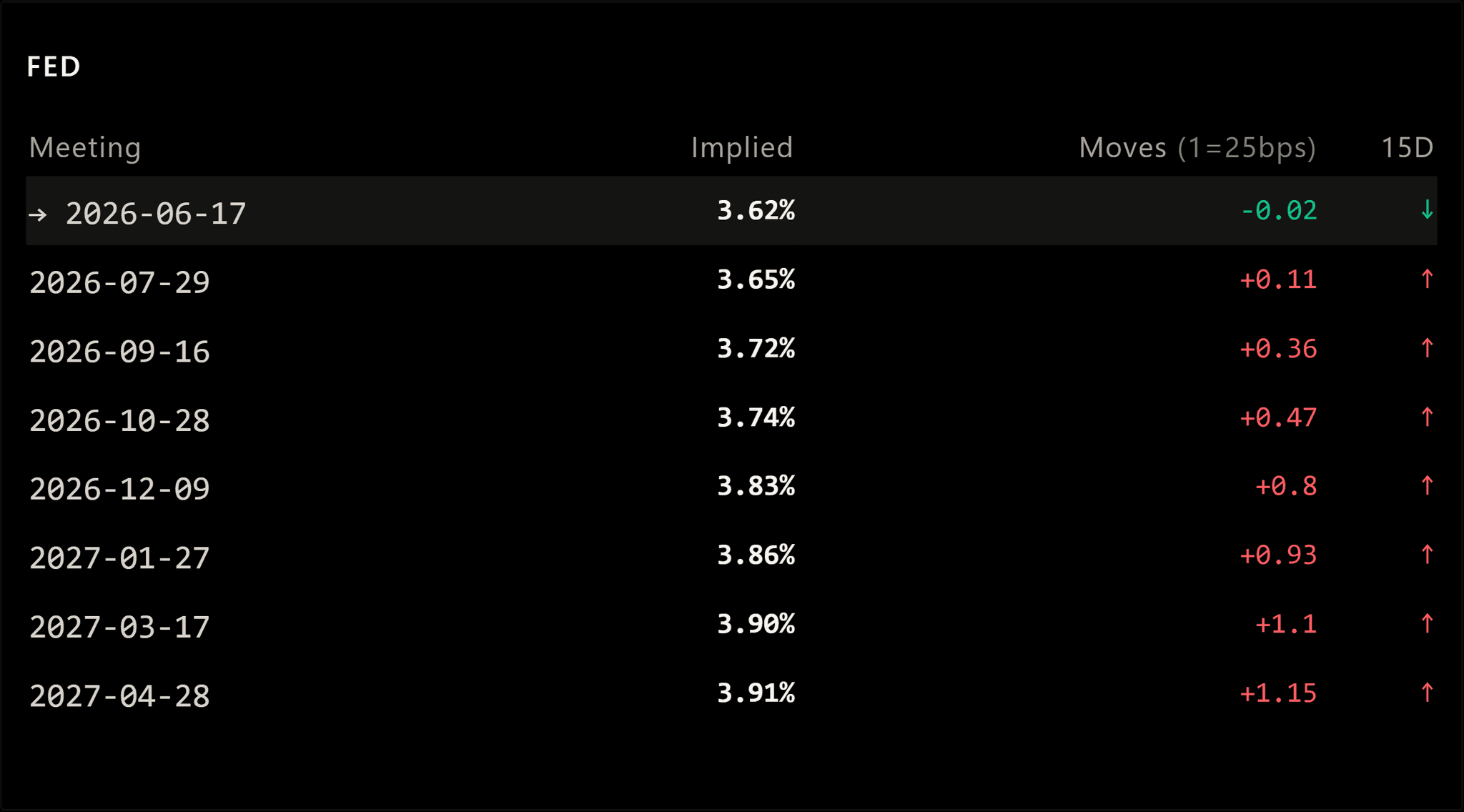

Fed funds futures recently came down from a full hike priced this year, now down to only an implied rate of 3.82% by December, with a full hike by Q1 2027. The Fed hasn't moved rates all year, yet the market has been tightening itself all year, with the Iran war weighing. The market priced the hikes. It can unprice them.

And it was never really about hikes. The hawkishness is the removal of cuts, not the pricing of a hiking cycle. The energy market was tightening the economy for the Fed, a non-stimulus inflation event, a supply shock that chokes demand on its own. That is why the Fed never had to move, and why a resolution puts market easing back on the table; it's not even about pricing in rate hikes, it's about being more lenient on the cuts that were just priced in.

Stimulus Without a Cut

The peace deal pulls energy out of the inflation path, and the curve has no reason to hold a near-full hike once its driver is gone. The path falls toward flat, the 2-year drops, mortgage spreads compress, and multiples re-rate on a lower discount rate. The market stopped pricing a war, and the economy gets the easing through a healthier consumer.

Join the Radar community

Create a free account to preview the QuantBase Terminal and get notified when new posts go live.

No spam · No credit card · Instant access

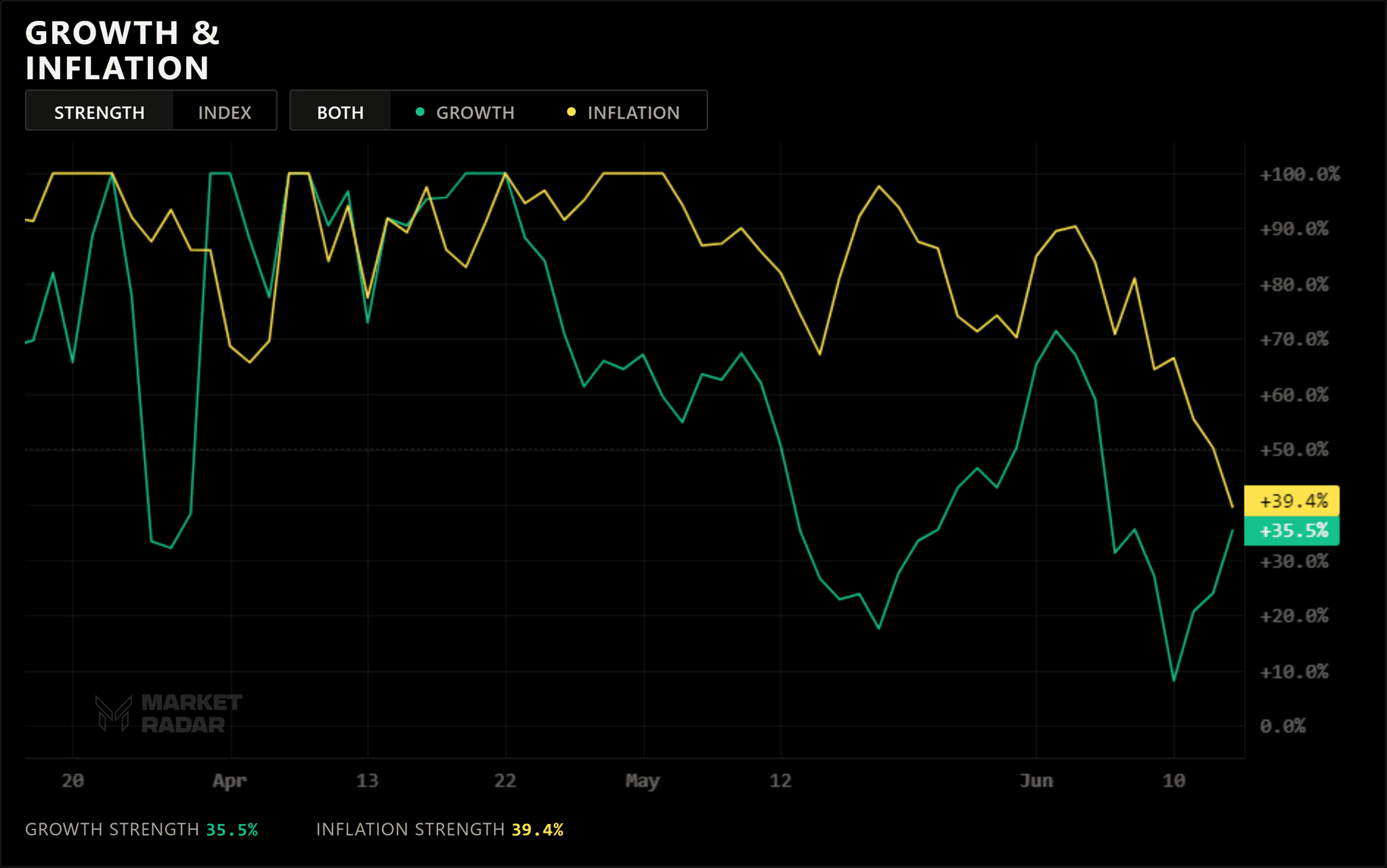

The deeper point is the inflation itself. A supply shock that pushes prices up chokes demand, so it tightens. Now running it backwards and falling supply-driven inflation is stimulative, because the demand restrictor comes off. We can't go back to an inflation regime from here, because we can't run one at $70 oil. A fresh inflation leg means crude back to $100 or $150, and that isn't the melt-up; that is proper stagflation. Holding the Inflation quadrant for the last three months instead of breaking into stagflation was close to a miracle. The inflation index has climbed at a 45-degree angle since December, along with growth, but in late April, growth decoupled from inflation. This suggests that inflationary impulses are beginning to hurt growth. We want to see inflation impulses continue to decline while growth remains elevated. This would take us into an Expansion regime and a sustained, healthy bull market with a consumer unburdened by excessive inflation.

Consumer + AI loop

The AI loop is still spinning, and underneath it, the tape is broadening: small caps and the equal-weight have turned on the Mag-7, industrials are the strongest corner outside the semis. The names that don't touch the AI buildout continue to underperform. We are still mid-CapEx cycle, and as long as the hyperscalers keep spending, it’s hard to manufacture a recession. The above trend inflation with positive growth all year worked because the inflation was supply-driven, not demand-driven. Put a reopening consumer on top of a loop that never needed one, and that is the real melt-up. Clean the energy shock off, and the inflation impulse collapses far enough to open a 3 to 6 month run, a deep Expansion regime rather than a narrow one. Inflation regimes are narrow growth with high prices. Expansion is broad growth with fading inflation impulses.

Growth is real, but it is borrowed. It only becomes a durable bull market if we can get into Expansion, and that hinges on one variable: energy. If the deal holds and crude keeps bleeding, the inflation impulse collapses, the demand restrictor lifts, and the consumer that has carried the cost of this entire regime finally gets unburdened, helping boost growth further. If the deal breaks and energy re-spikes, there is no comfortable inflation melt-up waiting on the other side. There is only stagflation, the road the System was already traveling before the peace deal. We wait for the model to confirm, and we watch energy. The stimulus arrived without a cut. Now the economy has to earn the rest.

Here's what our System says, and what trades we are anticipating:

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

Billed annually at $780 · Save $120

- Models boasting 40%+ average yearly returns

- Automated portfolio signals (RQF strategy)

- Live calls with experienced traders

- QuantBase Terminal with macro regime models

- DDAP TradingView indicator

- Real-time portfolio updates

- Private Discord channels